Part 3 of a Series

Creating Alpha in Private Credit

Adding Value via Capital Solutions

Key Takeaways

- Experienced private credit GPs can add value beyond asset performance by providing capital solutions that include customizing fund structures and dynamically optimizing funding and leverage of a private credit fund over its life cycle. This is an often-overlooked source of value creation that can have a significant impact on fund returns.

- Providing such return-enhancing capital solutions requires a combination of differentiating elements of scale, in-house expertise, strong relationships and a low cost of capital that only some GPs possess.

The Bottom Line

Most private credit managers focus on asset performance to drive alpha – selective underwriting, portfolio diversification, effective portfolio monitoring, and managing risk through cycles – as discussed in Part 1 and Part 2 of our “Creating Alpha” series. Asset performance is of course critical to adding value, but it is also table stakes. In the journey from fund formation to exit, Antares seeks to achieve a differentiated capability that benefits investors: an integrated, in-house structuring and financing capability that actively creates value throughout the lifecycle of a fund.

At Antares, we believe providing capital solutions over the lifecycle of a fund can also be a meaningful source of return enhancement.

Digging Deeper – Creating Alpha Over the Lifecycle of a Fund

Antares believes that alpha can be created throughout all stages of the fund lifecycle. This starts at the formation stage, continues as the fund deploys and then reinvests, and culminates in fund wind-down. By offering efficient fund structures, leverage solutions and exit strategies to its investor base, Antares seeks to “create alpha” for its partners throughout each phase of their investment with us.

Exhibit 1: Creating Alpha Over the Lifecycle of a Fund

| Formation | Initial Leverage & Fund Ramp | Investing/Harvesting | Fund Wind Down/Exit Opportunities |

|---|---|---|---|

| Asset Warehousing & Fund Structuring | Fund Leverage (ABLs & Sub Lines) | CLO Financing | Continuation Vehicle Credit Secondaries |

| Warehouse and build a diversified seed portfolio to reduce cost to investor and mitigate J-curve. Optimize fund structure for differing investor types and geographies. | Secure market-leading Asset Based Lending (ABL) & Subscription Line (sub-line) facility terms to minimize financing costs. Leverage can be effective as soon as seed portfolio comes in, if sufficiently diversified. | Lower cost CLO financing can takeout ABL financing 12-24 months after initial ramp. Impact can be material to a funds relative cost of capital for best-in-class CLO issuers. | Offering liquidity options adds value to drawdown funds near end of life or even to perpetual funds if investors desire accelerated liquidity. Impact highly bespoke and reflective of capital redeployment opportunities |

Fund Formation

We believe expertise in fund structuring is critical to put in place structures that optimize efficiency for multiple types of investors. Additionally, fund formation can also be a significant source of cost for investors in the form of legal bills so managers that can deliver these capabilities at least partly in-house can offer significant cost savings to investors and thus higher expected returns.

Adding value via a customization of the investment program involves identifying and solving for a myriad of investor requirements and preferences, which we think can include, but is not limited to:

Fund Type

Whether an investor experience is based off a structured note, a separately managed account, a fund of one, a comingled product.

Domiciliation

What jurisdiction(s) must a program or fund operate in and in what currencies satisfy the investor’s investment profile? There are evolving political and regulatory events that shift where certain funds may want to be domiciled and understanding the latest state of play on which domiciles may be favorable and investor preferences or regional regulatory requirements allow for dynamic structuring during the design of the fund.

Investment Guideline Customization

Balancing investor(s) investment mandates’, preferences and expected performance.

Capital Efficiency

Understanding what types of capital charges (internal or external) may apply or limit the investor’s experience and determining whether structured products and rating technology would address capital charge concerns.

Insurance: NRSRO-rated products to optimize capital efficiency for insurance investors. Antares maintains an in-house structuring team that can set up such structures directly with rating agencies without involving intermediaries. The expense savings are directly passed on to the investors.

Tax Matters

Understanding applicable tax treaties (if any), construction of tax guidelines, tax principles of different structures and available elections to help ensure the fund’s operation in a tax efficient manner.

Economics

Understanding investor’s requirements and preferences on manager remuneration – customizing fees to allow for specific incentives, “flat” fees, and other management fee levers.

Understanding investor requirements and preferences on the fund’s day-to-day activities and how it may impact fund expenses and performance.

Liquidity/Duration

Understanding whether the investor(s) require a fixed term (and its maximum duration), evergreen, or a hybrid

Fixed Term: The traditional total “term” (i.e. duration) of a fixed term fund is generally 7 to 11+ years which has historically allowed investors to capture the full illiquidity premium for having had their capital locked up.

Evergreen: The traditional evergreen fund does not have a specified “investment period” and “harvest period” but allows a fund to be continually in an investment period. Understanding the subsequent investor and exit options is critical to building an evergreen product that can truly remain open in most circumstances. Generally, understanding the liquidity and exit options preferred by the investor(s) allows for the structure to balance gates, shorter soft lock up periods, and fast and slow pay ramps to optimize performance in a more liquid product.

Risk Mitigation

In balancing the above considerations (amongst others), ensuring the LP is able to diligence, report, and otherwise satisfy their own internal investment requirements and risk profile.

Financing

Just as strong origination capabilities are critical for sourcing deal flow in the private credit loan market, maintaining strong and diverse relationships with lenders is critical from a fund financing perspective for sourcing and managing leverage commitments. When sourcing financing for a fund, particularly from banks, the ability to lean on strong institutional relationships and draw on a large set of potential lenders incentivizes lenders to put their best foot forward and enables negotiation of market leading terms. Managers with scale often do regular and repeat business with the largest, most reliable lenders in the space. As a result, lenders are often willing to offer better terms in order to keep getting access to future business given the long-term partnership.

At Antares, we leverage the strength of our underwriting track record and workout capabilities, among other factors, to help secure attractive financing terms.

Exhibit 2: Creating Alpha with Analytics – Capital Strategy

Effective fund structuring and management requires good judgment and expertise, but also a strong analytical foundation. A key source of alpha generation is the ability to effectively leverage sophisticated, proprietary analytical tools in key areas, including:

Capital Strategy: a typical private credit fund has liabilities in the form of unfunded asset commitments and, in the case of levered funds, potential “revaluation,” or a requirement to put additional equity capital into the fund’s leverage facilities. To make sure these obligations can be met, the fund must always reserve a portion of its equity commitments or other fund capital. By using a comprehensive model to determine the amount of capital needed in downside scenarios based on historical activity, the manager can monitor these exposures in real time to ensure the appropriate amount of capital is reserved. In the case of drawdown funds, this is critical to maximizing deployment of investor’s capital, and in the case of closedend funds (such as BDCs), which generally rely on availability under bank financing facilities rather than uncalled equity commitments, this is critical to managing to target leverage while ensuring the fund can meet its target return objectives.

Asset Based Lending Facilities (ABLs)

ABLs act as an initial source of leverage and asset purchasing power for private credit funds. Managers with the strongest lender relationships, highest credit quality and most diverse portfolios can often command the lowest pricing and most borrower-friendly terms, which can be a significant return driver.

The ABL structure can vary, and we expand on a few key terms in the next section, but the primary usage of ABLs is to increase a fund’s purchasing power and drive levered returns for the fund. As an example, a private credit fund can expect to receive ~70% of an asset’s principal balance in debt proceeds from its ABL. The remaining 30% of the asset’s principal balance is funded with equity commitments from the fund. By borrowing the other 70% of the asset’s principal balance from a bank, a private credit manager increases the purchasing power of the fund by leveraging the debt proceeds to purchase incremental assets.

Subscription Facilities – Sub-lines and Swinglines

Another common financing product that can be an important part of a fund’s financing strategy are subscription facilities

(“sub-lines”). Sub-lines can alleviate the operational burden on investors to fund several capital calls throughout the investment period of a fund by having the sub-line lender front those capital calls using the investor’s commitments to the fund as collateral. A sub-line can thus allow the GP to plan fewer and consistent capital calls to the investors of a fund without interruption to the fund’s capital needs. Sub-lines are typically offered by banks, oftentimes the same banks that are active in the ABL market.

The terms of a sub-line are driven by the lender’s view of the creditworthiness of the investors. For example, the lender may be willing to lend a higher amount against an investment grade rated investor vs. an unrated family office, due to the perceived counterparty risk of each investor’s uncalled capital. Managers can work with sub-line lenders when negotiating the sub-line terms to ensure that the highest possible advance rate is achieved relative to the credit worthiness of the fund investors.

As a fund ramps and the amount of uncalled investor commitments decreases, managers can proactively downsize sub-line commitments to minimize fees charged on the sub-line and improve fund returns.

In addition to ABLs and sub-lines, there are a multitude of additional financing products that can also be beneficial to fund performance where applicable. For example, corporate revolvers, unsecured bonds and repo agreements are other forms of financing that can be a key part of a fund’s financing strategy. The usage of these financing vehicles is specific to different

funds’ investment mandates and liquidity management considerations. At Antares, we believe we have deep experience in each product and continuously evaluate all financing options to create the best outcome for our fund investors.

Investing/Harvesting

Fund structuring does not end after the fund closes. It is important to continually evaluate and optimize a fund’s financing as the market evolves and the fund matures. This can include opportunistic refinancings, amendments to deal terms to provide additional flexibility to manage the portfolio, or simply a different type of financing structure.

“CLO take-outs” are one of the most common and beneficial strategies to optimize a fund’s financing structure after it has ramped. Once a fund is ramped (or is at least partially ramped), significant revolving capacity (a key feature of ABLs) is no longer needed, so the ABL can be “taken out” or replaced with a term financed CLO structure by transferring the assets from the ABL to a CLO and using the proceeds of the CLO to pay down and/or terminate the commitments of the ABL facility.

Advantages of CLO financing include:

- Pricing: Typically, CLO pricing is lower than ABL pricing (through an equivalent advance rate) because the wider investor base increases demand, CLOs are fully funded, and there’s greater liquidity.

- Leverage: CLOs can be structured with several classes of sequential-pay tranches to customize the amount of leverage applied to the collateral. While ABL facilities typically have a maximum 70% advance rate, CLO funds can achieve an advance rate of 85%+.

- Non Mark to Market/No Margin Call Structure: Declines in asset value do not require the fund to put in more capital through a margin call. If there is material underperformance, the CLO may begin to de-lever.

- Tenor: CLOs typically have a maturity 8 years after the end of the reinvestment period, exceeding the maturity of the assets in the CLO, so there is minimal funding risk as the portfolio ages. ABLs typically have a reinvestment period of 3 years, with a maturity 2 years after the end of the reinvestment period.

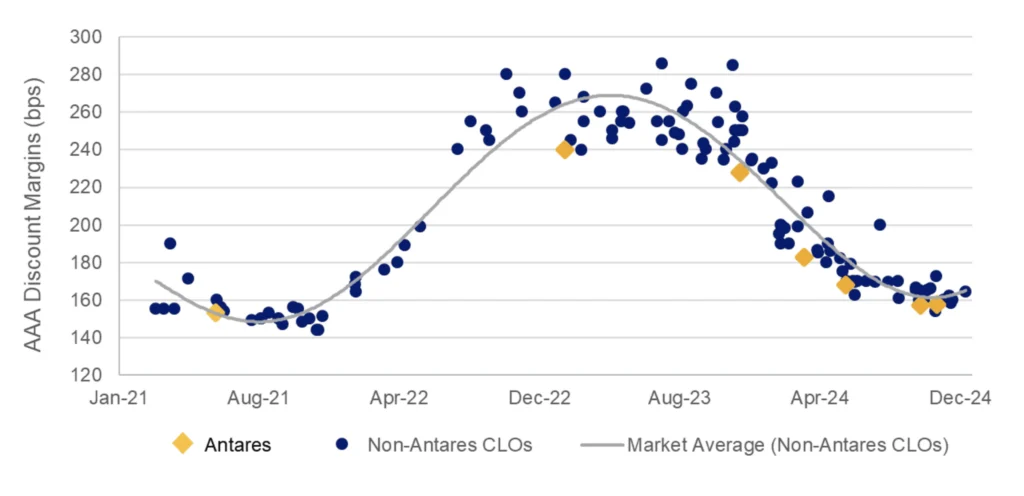

Access to the CLO market is not a given – it is dependent on having capital markets relationships, scale and a long track record of managing CLO structures – something that cannot be easily replicated. The few largest players in the private credit space dominate CLO market issuance and smaller players are often not able to command enough investor demand to issue in the CLO market or at attractive pricing. Scale also enables consistent issuance, which is critical to sustaining the engagement needed to have a CLO investor base. The five largest CLO managers accounted for 37% of total issuance in 20241.

Similar to the ABL market, pricing in the CLO market can vary materially by manager depending on their track record and the quality of their assets. For example, Antares is one of the largest private credit CLO issuers and has historically achieved market- tight CLO pricing, as shown in Exhibit 4. The impact of lower cost of funds on a funds returns can be material. For example, for a 2x levered CLO, a 25 bps lower cost of funds can improve returns by ~40bps which is significant for a low levered loan strategy. In the case of higher leverage, the impact on fund returns would be expected to be greater.

Exhibit 3: Antares Private Credit CLO AAA Spreads vs. the Market2

Exhibit 4: Creating Alpha with Analytics – Transaction Analysis

Transaction Analysis: as discussed in previous sections, optimizing fund performance requires continually evaluating and seeking new options for the financing on a levered fund, particularly as the fund becomes ramped (see “CLO Takeouts”) or approaches or passes the end of its reinvestment period. Once these opportunities are sourced, rigorous analytics are needed to determine if the alternative financing will be accretive to the fund. A comprehensive return model that appropriately accounts for the nuances of financing structures is needed, as well as the ability to run scenario analysis to see if the new financing is expected to be superior across multiple possible scenarios, including default rate environments, interest rate environments, prepayment rates, and more. With a plethora of analytical results, the manager is in the best position to decide on the optimal financing strategy for the fund and execute accordingly. In addition, the model can be used to help negotiate deal terms by narrowing down terms that are most valuable to the fund’s performance and focusing on those with financing providers.

While decision making is generally qualitative, quantitative metrics help guide decision making to ensure decisions are accretive to the fund.

Exit Strategies – Liquidity Solutions and the Growth of Credit Secondaries

Continuation Vehicles

Private credit GPs generally aim to hold their loan investments to maturity and therefore, a portion of loans within a fund’s portfolio that aren’t paid off early or refinanced away will go through a harvest period until they reach maturity. However, once a fund’s investment period is over, investors often want to get their capital back as quickly as possible to re-deploy into new funds. In order to solve for this liquidity need, a continuation fund can be created by the GP to purchase assets from the legacy fund, allowing LP investors in the legacy fund the option of cashing out or reinvesting (i.e. roll over) into the new continuation fund along with new investors.

Continuation vehicles can also be created out of large, diversified portfolios well before the end of a fund’s life. These are less common and may reflect the sale of a subset of a portfolio that would benefit from being repackaged or re-leveraged, or to meet certain investor needs.

LP-led transactions

LPs may seek liquidity for their interest in a fund near or before the end of fund life for any number of reasons, such as the need to rebalance their asset allocation (e.g. the “denominator effect”) or to satisfy other LP goals or obligations. In this case, LPs can sell into the credit secondaries market which is still relatively nascent but growing rapidly. Antares’ Credit Secondaries investment strategy has been expanding to serve such needs and will focus on both GP-led and LP-led credit secondaries opportunities leveraging the firm’s extensive private credit and structuring expertise.

Conclusion

At a time when the private credit market is growing more crowded and investor expectations are rising, the ability to create alpha beyond asset origination and portfolio management is a clear differentiator. Antares does not just create alpha via loan underwriting and portfolio management — we also design fund structures, financing strategies, and exit solutions that seek to enhance investor outcomes.

For our LPs, that means partnering with a manager that seeks to deliver alpha in every aspect of the solutions we provide.

Footnotes & Disclosures:

Reflects Antares’ beliefs unless otherwise cited with a source.

1Source: Creditflux Middle Market CLO Issuanca as of December 31, 2024. Five largest CLO issuers in rank order as listed were Antares, Blue Owl, Ares, Cerberus and Golub.

2Source: CreditSights CLO Databank. Data includes all US new issue CLOs that have priced between January 1, 2021 – December 31, 2024, excluding deals with reinvestment periods of 3 years or less, broadly syndicated loan CLOs, and static pool CLOs. Middle market CLOs generally price wider than broadly syndicated loan CLOs (“BSL CLOs”), and static pool CLOs typically price tighter than BSL CLOs. Please note that the dataset represents the discount margin (“DM”) at time of the respective deal pricing, as reported by CreditSights CLO Databank. CLOs that have not reported DMs are not included in the dataset. Antares Capital Advisers dataset represents the AAA DM of each respective deal at pricing, as reported by CreditSights CLO Databank. Past performance is not a reliable indicator of future performance and future results may differ materially. Market average is based upon a polynomial order 6 statistical trend line as calculated by Excel. Includes both private credit CLOs that are consolidated on the Antares balance sheet as well as private credit CLOs that are not consolidated on the Antares balance sheet of December 31, 2024. CLOs consolidated on the Antares balance sheet have historically experienced favorable impacts from financial support provided by the Antares balance sheet and CLOs that are not consolidated on the Antares balance sheet may not be managed the same way.

The materials presented herein are provided to you solely for informational purposes and unless otherwise indicated herein, has been prepared using, and is based on, information obtained by Antares Capital (“Antares”) from publicly available sources. It does not constitute an agreement, or an offer, commitment to offer, or agreement to sell any loans, securities or other assets including interests in any fund or vehicle. The materials contained herein are not intended, nor should they be construed or implied, to be a recommendation or advice of any kind. The information set forth herein has been compiled as of the date(s) noted, is preliminary and subject to change. There is no obligation on the part of Antares to update the information provided herein after the date hereof. Neither Antares nor any affiliate thereof represents or warrants the accuracy, completeness or reliability of any of the materials contained herein, either expressly or impliedly, for any particular purpose, and shall have no duty to update or correct any such information. Without in any way limiting the generality of the foregoing, you understand that certain of the information provided herein is based on information provided by third parties, and neither Antares nor any affiliate thereof makes any representation or warranty regarding the accuracy, completeness or reliability of any such information. In no event will Antares be liable for any losses or damages arising from or as a result of the use of the information or the materials contained herein.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Antares believes that such information is accurate and that the sources from which it has been obtained are reliable; however, none of Antares nor any of its affiliates or agents can guarantee the accuracy of such information and they have not independently verified and are not responsible for any inaccuracies, omissions and outdated information contained in such third-party information or the assumptions on which such information is based. Certain other information regarding market analysis and conclusions could be based on opinions or assumptions (including those of Antares) that Antares considers reasonable. Unless otherwise indicated, such market analysis and conclusions represent the subjective views or beliefs of Antares.

The materials presented herein may include certain projections, forecasts and estimates that are forward-looking statements. Any such forward looking statements are based on certain assumptions about future events and are subject to various risks and uncertainties. Forward-looking statements are necessarily speculative in nature and it should be expected that some or all of the assumptions underlying them will not materialize or will vary significantly from actual results. Accordingly, actual results will vary from the projections, and such variations may be material. Some important factors that could cause actual results to differ materially from those in any forward-looking statements contained in these materials include, without limitation, changes in interest rates, default and recovery rates, market, financial or legal uncertainties, the timing of acquisitions of loans, the types of loans acquired, differences in the actual allocation of loans from those assumed mismatches between the time of accrual and receipt of interest proceeds from the loans and whether or not and how loan investments may be leveraged.

Any statements involving matters of opinion or estimates, whether or not so expressly stated, are set forth as such and not as representations of fact, and no representation is made that such opinions or estimates will be realized. The statements and expressions of opinion contained in this presentation are subject to change without notice and involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon nor should they form the basis of an investment decision.

For Benefit Plan Investors

Not in limitation of the foregoing, if you are (or are acting on behalf of) a person that is a “benefit plan investor”, as defined in Section 3(42) of ERISA and DOL regulations (“Benefit Plan Investor”) you are not authorized to, and should not, rely on any information Antares is providing to you as a basis for, or otherwise in connection with, making a decision whether or not to invest with Antares. Antares has not provided and will not provide any investment advice of any kind whatsoever (whether impartial or otherwise) and Antares is not acting as a fiduciary, within the meaning of Section 3(21) of ERISA, and regulations thereunder, to the Benefit Plan Investor or to any fiduciary or other person making investment decisions on behalf of the Benefit Plan Investor, in connection with these materials or any related presentation.

Additional Matters and Important Information for All Non-U.S. Investors

An interest in products or services referenced in this presentation may not be licensed in all jurisdictions, and unless otherwise indicated, no regulator or government authority has reviewed this document or the merits of the products and services referenced herein. If you receive a copy of this presentation, you may not treat this as constituting a public or other offering and you should note that there may be restrictions or limitations to whom these materials may be made available. This presentation is directed at and intended for institutional investors (as such term is defined in the various jurisdictions). This presentation is provided on a confidential basis for informational purposes only and may not be reproduced in any form. Before acting on any information in this presentation, recipients should inform themselves of and observe all applicable laws and regulations of any relevant jurisdictions. Recipients should inform themselves as to the legal requirements and tax consequences within the countries of their citizenship, residence, domicile and place of business with respect to the ongoing provision of services, and any foreign exchange restrictions that may be relevant thereto. Antares does not accept any responsibility, nor can be held liable for any person’s use of or reliance on the information and opinions contained herein. Any entity responsible for forwarding this material to other parties takes responsibility for ensuring compliance with applicable securities laws.

Notice to persons in the European economic area and the United Kingdom

This presentation is being made available: (1) to persons in the European economic area only if they are professional investors as defined in the Alternative Investment Fund Managers Directive (2001/61/EU); and (2) to persons in the United Kingdom only if they are professional investors, as defined in the Alternative Fund Managers Regulations 2013 and fall within the following categories of exempt persons under the Financial Services and Market Act (Financial Promotion) Order 2005 (the “FPO”) and the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemptions) Order 2001 (the “CISPO”): (i) persons who are investment professionals, as defined in article 19(5) of the FPO and article 12(5)of the CISPO; (ii) persons who are high net worth companies, unincorporated associations etc., as defined in article 49(2)(a) to (d) of the FPO and article 22(2)(a) to (d) of the CISPO; or (iii) persons to whom it may otherwise lawfully be communicated. This presentation is provided for informational purposes only and does not constitute as offer to purchase, acquire, or subscribe for any type of investment.