The Next Frontier in Private Credit Secondaries

The asset class is entering a new phase involving larger, more complex opportunities that are increasingly central to how investors manage risk and liquidity in an illiquid world.

Key Points1

- Once a nascent market, the private credit secondary market is an important channel for investors to manage risk and unlock liquidity across complex portfolio exposures.

- During its initial period of opportunistic growth, private credit secondary participants could simply “buy the market” through broad pursuits, gaining and maintaining market share by acquiring assets at scale.

- Credit Secondaries 2.0 will be marked by selective underwriting and structuring innovation, along with the ability to deliver flexible capital solutions.

- For investors, it’s becoming increasingly important to work with managers in this specialized market segment that have extensive sourcing relationships, structuring expertise, and deep experience navigating through the complexities of credit markets and through different market environments.

Introduction

Two decades ago, private credit—once a niche market of non-public loans to private companies—was relatively small and loosely defined. At the time, most privately held businesses relied primarily on traditional bank financing to fund growth and operations. Only a handful of companies, such as Antares Capital, founded in 1996, focused on originating and structuring loans for private equity–backed middle market businesses that sought alternative financing options to conventional bank loans.

In the aftermath of the Global Financial Crisis, which triggered a wave of consolidation in the banking sector, banks no longer had the ability (due to changing regulations) nor the appetite to hold loans on their balance sheets to the degree that they once had. Back in 1994, banks accounted for 71% of primary market leveraged loan purchases.2 By 2022, they accounted for just 12% of the market.3

The banking sector’s retrenchment came amid growing interest in alternative private investment opportunities from institutional investors. Both factors opened the door to private credit and ushered in years of significant growth. By 2018, the private credit market had topped $1 trillion and continued to grow by a 17.5% compounded annual growth rate through 2023.4 By 2028, this market is expected to reach $2.8 trillion.5

As with private equity (“PE”), the growth of the secondary market was initially driven by aging fund portfolios, where traditional exit paths—such as M&A, IPOs, or sponsor-led exits—failed to materialize within expected timelines. This was compounded by prolonged holding periods, diminished exit activity, and liquidity mandates pressing against limited distribution flows. In the first quarter of 2025, PE exit values were the lowest in five years as mergers, acquisitions, and initial public offerings experienced a marked slowdown6. These dynamics accelerated the continued growth of PE secondaries as investors sought alternative avenues for liquidity and portfolio rebalancing. In parallel, private credit secondaries emerged to address similar challenges, as investors look to monetize or actively manage seasoned credit portfolios where underlying loan quality remains strong, but realizations are increasingly delayed. The effective loan life of direct loans has subsequently lengthened to almost four years after being below three years for most of the decade preceding COVID-19.

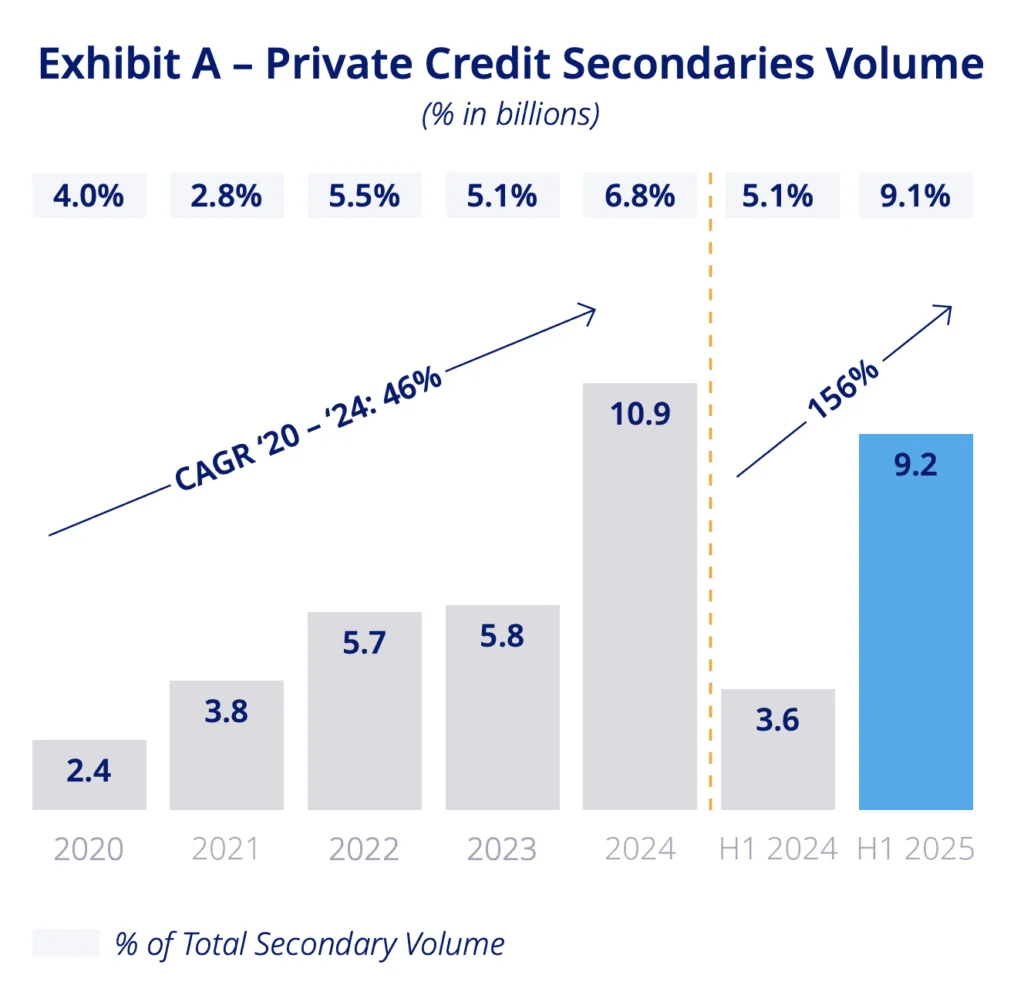

What began as a niche play has rapidly evolved—today, the private credit secondary market is nearing an inflection point in scale and investor interest. U.S. activity is largely driven by direct lending, with volume reaching $9 billion in the first half of 2025, a 156% year-over-year increase7 as shown below.

Yet, credit secondaries still represent only ~9% of total secondary market volume8 and just ~1% of the $1.6 trillion in North America-focused private debt AUM9. With private credit AUM projected to grow at a 11% CAGR over the next five years10, even a modest rise in credit secondary penetration to 1–2%— compared to ~3% in private equity—could drive annual volume to $30–60B by 2030. Broader inclusion of adjacent segments such as asset-based lending (ABL), real estate and infrastructure credit, and investment-grade private credit would further expand the opportunity set. As the market evolves, what it takes to source and analyze opportunities, and deliver on behalf of different investor types, is dramatically changing.

Solving for Liquidity

To date, the roughly decade-long growth of the private credit secondary market could be defined as its initial stage. During this period of opportunistic growth, participants could simply “buy the market” through broad and indiscriminate pursuits, gaining and maintaining market share by acquiring assets at scale without deep differentiation in terms of credit quality, duration, and pricing, among other factors. In this sense, the private credit secondary market evolved much in the same way the one for PE secondaries did.

But we believe there are some critical differences in the benefits that private credit secondaries provide over their PE counterparts. While both involve the buying and selling of existing investment interests, buyers of private credit secondaries generally earn most of their total return from the current income the investments generate, whereas PE investors must rely on appreciation realized from harvested investments. This greatly reduces the risk of loss for private credit investors, who tend to be far more focused on earning a competitive rate of return versus risk of recouping their initial capital.

Still, if loans are not paying off as quickly as expected—because exits or M&A are delayed—LPs may face slower capital return and reduced ability to recycle capital across commitments, despite getting regular coupons from the interest. While these fully deployed portfolios generate current income, a LP may seek to sell fund interests to rebalance exposures across strategies and managers, manage duration or liquidity needs and shift vintage exposures.

This waterfall dilemma is one of the key drivers behind the growth of the private credit secondary market, but not the only one, as we discuss the manifold benefits of secondaries below.

Distribution Waterfalls

In credit secondaries, investors face the “waterfall” consideration, where ongoing interest and principal repayments are distributed throughout a fund’s life. Unlike private equity, where value is typically realized at exit, credit portfolios return capital steadily—meaning much of the return may be paid out before a secondary investor enters.

Yet, this dynamic also can create key advantages. Investing in seasoned, cash-flowing portfolios offers immediate current income, reduced J-curve exposure, and access to performing credit assets with downside protection. When combined with thoughtful pricing and efficient structuring, credit secondaries provide institutional investors a differentiated way to access liquidity, manage allocations, and capture total return from resilient credit portfolios.

| Transaction Type | Initiator | What’s Transferred | Purpose |

|---|---|---|---|

| LP-Led | LP | Fund Interest | Liquidity, rebalancing |

| GP-Led – Continuation | GP | Loans/assets into new vehicle | Extend hold, provide LP optionality to crystallize returns, liquidity |

| GP-Led – Strip / Asset Sale | GP | Slice of assets to external buyer | Portfolio management, liquidity |

| Direct Loan Portfolio Sale | Manager, Bank, BDC | Loans (performing/stressed) | Rebalance exposure, manage leverage, balance sheet liquidity |

| NAV-Based Lending | GP or LP | Secured loan against portfolio NAV | Liquidity without asset sale, enhancing DPI |

Continuation Funds Explained

Continuation funds allow a fund’s general partner to transfer one or more performing assets from a maturing fund into a newly formed vehicle, while offering liquidity options to existing investors. In private credit, continuation vehicles serve as a GP-led liquidity solution that optimizes outcomes for all stakeholders—granting LPs optionality, enabling GPs to maintain conviction positions, and opening opportunities for new capital to join a well-understood, performing credit portfolio.

LPs are increasingly looking for liquidity solutions to rebalance their portfolio allocations and the reasons for that could be very idiosyncratic. LPs may need liquidity due to the impact of dislocations in public market holdings, regulatory pressures, and/or the denominator effect in which a notable change in the value of one asset class disproportionately impacts the overall portfolio allocation forcing a rebalance. Others may be reallocating investments among strategies, managers and assets. These transactions comprise most of the volume of the credit secondaries market, accounting for an estimated 54% of volume in 2024.11

While GP motivations may vary—from raising capital for new funds or acquisitions to preserving dry powder for portfolio company support—these actions are ultimately guided by their fiduciary duty to act in the best interests of their investors. As stewards of capital, GPs aim to deliver optimal execution, pricing, and long-term returns. In today’s environment, where private equity firms are holding assets longer due to slower exit activity, repayment timelines for private credit loans are also extending. This dynamic can impact liquidity and duration for investors in private credit funds, making effective secondary solutions and proactive portfolio management even more critical. GP-led transactions contributed an estimated 46% of credit secondary deal volume in 2024,12 and they are expected to rise in step with the growing market, especially if exits remain hard to realize.

Investors needing liquidity may turn to the private credit secondary market and find that credit secondaries offer lower bid-ask spreads than in private equity or in real estate, where the terminal value of long-duration assets is much harder to assess. That is because, if properly vetted, the underlying credit provides a predictable, steady stream of income. For a seller with illiquid assets, this is immediately appealing and helps explain the deepening of the market for private credit secondaries.

Credit secondaries offer a compelling entry point for investors seeking to manage duration risk while enhancing capital efficiency. Unlike traditional primary fund commitments, these investments provide immediate deployment into seasoned, income-generating assets—reducing blind pool risk and accelerating cash flow. Private credit secondary portfolios also tend to be well diversified across borrowers, sectors, and structures—offering broader risk dispersion than many private equity secondary opportunities, which are often more concentrated. Coupled with lower market correlation, reliable quarterly distributions, and the potential for consistently attractive risk-adjusted returns, credit secondaries serve as a strategic and resilient complement within a private credit allocation.

Credit Secondaries 2.0

We are now entering the next frontier of private credit secondaries—one defined not by who arrived first but by who brings the right capabilities. The market is seeing greater prominence from seasoned primary credit investors with the expertise to underwrite underlying assets and selectively price complex opportunities. Their deep underwriting experience, borrower familiarity, and structuring know-how offer a distinct edge in navigating the complexity and opacity that still characterize many secondary transactions.

At the same time, we have seen credit investors who may compete in primary underwriting and origination are increasingly comfortable allocating to one another’s funds—driven by aligned investment theses and the mutual need for scale, diversification, and transparency in sourcing and diligence. In this environment, success hinges on experience, structuring expertise, and rigorous credit diligence—capabilities that are critical to sourcing and executing complex secondary transactions. Differentiated access through proprietary GP and LP relationships, real-time borrower insight, and sector-specific intelligence all promise to enhance a manager’s ability to identify opportunities early.

Of course, some are better positioned than others to compete in this evolving market. Rising corporate debt, credit market dislocation, and changing regulations all combine to present favorable macro trends for those with strong capital bases. The potential for enhanced returns exists because of market volatility, which can lead to attractive discounted investment opportunities and grant an edge to managers with disciplined due diligence processes and experience. The illiquidity of private credit assets and information asymmetry create pricing inefficiencies, offering opportunities for experienced managers who can scale.

A sharp focus on asset performance remains essential, through selective underwriting, portfolio diversification, effective portfolio monitoring, and managing risk throughout a fund’s cycle. But those traits now amount to table stakes for performance.

As we enter the next phase of the market’s evolution, and as more competitors crowd into the market and investor expectations rise, new capabilities are required to create value. Going forward, leveraging disciplined underwriting, in-house structuring and fund finance design and evaluation, and deep credit expertise will be needed to navigate transaction complexity and capitalize on market inefficiencies across deal types, vintages, sectors and geographies.

Risk & Return Considerations

As private credit secondaries evolve into a more defined and active segment of the market, investors evaluating this space should focus on the factors that truly differentiate managers. We believe those key considerations include the ability to assess loan quality, navigate limited transparency, manage duration and concentration risks, and bring structuring expertise to complex transactions. Understanding how a manager addresses these elements is essential to making informed allocation decisions and the following are our insights into these considerations.

Assessing Performance in Credit Secondaries

Returns in a credit secondaries fund are primarily driven by generating immediate income from interest income, purchasing assets at a discount, and capturing upside as loans pull to par or repay early. Recycling repaid capital at attractive discounts during the investment period can enhance multiple on invested capital (MOIC), though reinvestment spreads and asset quality must be managed to preserve IRR. Duration plays a key role—shorter timelines can accelerate IRR, while longer holds may support a higher MOIC.

This differs from primary credit funds, where capital is deployed over a longer ramp-up period and return realization builds gradually as portfolios season. Viewed together, primary and secondary credit strategies can serve complementary roles in a portfolio, offering distinct duration and liquidity profiles. These differences can help investors fine-tune asset allocation and better align their pacing, income needs, and duration targets across market cycles.

Loan Quality

One of the faulty assumptions hovering over the private credit secondary market is that the positions being sold may represent deteriorating credit quality. In that respect the secondary market is no different from the primary market, and there are pricing opportunities that reflect the risk/reward disparity.

Even in the case of higher-quality credits, an investor may question why a general or limited partner would sell a well-performing loan generating an attractive return. The reality is that such sales are frequently driven by portfolio rebalancing objectives or liquidity needs, rather than underlying credit concerns.

As mentioned, there are a multitude of motivations that might be pushing a seller to raise funds. Therefore, one of the critical differentiators when sourcing deals is how well the manager knows the GPs and LPs who are offering the opportunity.

Transparency

Further, some investors have expressed concerns about the transparency of the secondary portfolios. While they have the benefit of seeing how these underlying funds have performed, which provides powerful insight into a loan portfolio, other information may not be readily available. Many private credit loans lack ratings and up-to-date mark-to-market pricing, for instance. Managers evaluating secondary offerings typically operate within a compressed timeline – often just four to six weeks – compared to the three months typically allocated for underwriting direct loans.

Due to this information asymmetry, partnering with a direct lender that has deep underwriting experience and understanding of the industries involved – if not direct familiarity with the individual borrowers – can be a significant advantage.

Duration

Opportunities in secondary private credit typically involve commitments that fall at the midpoint or later in a fund’s or loan’s lifetime. For some, this profile is attractive to those focused on accelerated cash flow and reduced J-curve exposure. For others, the shorter remaining duration may limit the long-term capital appreciation typically sought in earlier-stage investments.

Less mature assets include secondary acquisitions of relatively recent vintage funds or credit portfolios, often still deploying capital. These are appealing to those seeking growth and longer-duration exposure, though there is greater uncertainty in asset performance. On the other side of the spectrum are tail-end portfolios comprised by older vintage funds with limited remaining assets, often in wind-down or harvest mode. These investments can be appealing because they might offer fully funded portfolios, more certainty on the credit exposure, and attractive illiquidity discounts.

There are several ways to add duration to a fund. The first option is in the initial selection, looking for those assets with three-plus years of duration rather than those with, for example, 15 or 18 months remaining. The second option is by working with managers to focus on loans that can be extended or recycled. This requires close working relationships with a broad group of managers who have diversified holdings.

Diversification

Another factor to consider is how concentrated or diversified a secondary offering is, as the composition can drastically affect its risk- and-return profile.

Concentrated secondaries typically involve purchasing interest in a small number of credit assets or funds, often focused on one manager, sector, or strategy. These portfolios offer the potential for outsized returns through manager or asset selection and provide more control or influence over outcomes (especially in co-investment or direct credit deals). However, these investments inherently have higher risk due to limited diversification and require more due diligence to underwrite idiosyncratic exposure.

Diversified secondaries are acquisitions of large-scale funds or a broader pool of LP interests across multiple funds, vintages, and managers. While these portfolios offer risk mitigation through diversification, they may offer lower potential for alpha and can include less-desirable assets, or blind pool risk.

Structuring

Complex secondaries are deals involving more bespoke or structured transactions, such as GP-led restructurings, strip sales, preferred equity, or securitizations of credit assets. Due to the complexities described above, there is greater execution risk and due diligence than with traditional secondaries, though experienced buyers can tailor their risk/return profile and sometimes generate higher IRRs.

A growing and critical area to provide liquidity solutions exists in securitizations, including CLOs, CFOs, and rated feeders and rated notes. These solutions repackage portfolios of borrowers, funds, or loan stakes and issue securities backed by the anticipated cash flows of those interests. The investments can be split into tranches with varying risk/return profiles and can deploy leverage to enhance returns. A well-structured securitization could broaden the investor base for these products; risk-averse investors such as insurers can buy senior tranches, whereas credit specialists might be drawn to junior tranches.

Staying at the Forefront

The market for private credit secondaries shows no signs of slowing down as it matures and enters a new phase. We do not believe it is important which firm arrived first and claimed stakes to market share by buying into the asset class. The market shift will favor seasoned primary credit investors with the expertise to underwrite and selectively price complex opportunities. Many private credit secondaries remain characterized by complexity and opacity and those with deep underwriting experience, borrower familiarity, structuring know-how, and rigorous credit diligence can navigate through the hurdles—and source and execute complex secondary transactions.

We believe the next phase of private credit secondaries will reward those who bring credit expertise, real alignment, and the infrastructure to act with speed and conviction. Antares, drawing on its long-standing tenure as an original private credit investor, is well situated to identify and understand the nuances of the market and how to navigate its complexities. With decades of experience across cycles, we have unmatched experience, structuring expertise and credit diligence capabilities.

Footnotes

1 Statements reflect Antares’ beliefs.

2 Milken Institute, The U.S. Leveraged Loan Primer (October 2004)

3 Franz J Hinzen, Nonbank Market Power in Leveraged Lending (October 2023)

4 BNY The Inexorable Rise of Private Credit ( June 2024)

5 Preqin, Future of Alternatives 2028 Report (October 2023)

6 Pitchbook Q1 2025 PE Middle Market Report (April 2025)

7 Evercore 1H25 Secondary Market Review ( July 2025)

8 Evercore 1H25 Secondary Market Review ( July 2025)

9 Preqin North American Private Debt AUM data as of December 2024 (funds only, excludes BDCs) of $1.095T plus $475B of BDC AUM as per LSEG LPC Middle Market Connect 1Q25 BDC Analysis (May 2025).

10 Preqin’s Future of Alternatives 2029 report (September 2024)

11 Jefferies Private Capital Advisory Global Secondary Market Review (January 2025)

12Jefferies Private Capital Advisory Global Secondary Market Review (January 2025)