Navigating Private Credit’s Next Chapter

Key Takeaways

Private credit remains a story of consistency and opportunity:

- Direct lending performance has been strong as measured by the CDLI at 6.7% YTD-3Q25, overperforming leveraged loans but slightly behind high yield. The CDLI appears to be on pace to return near 9% unlevered in 20251.

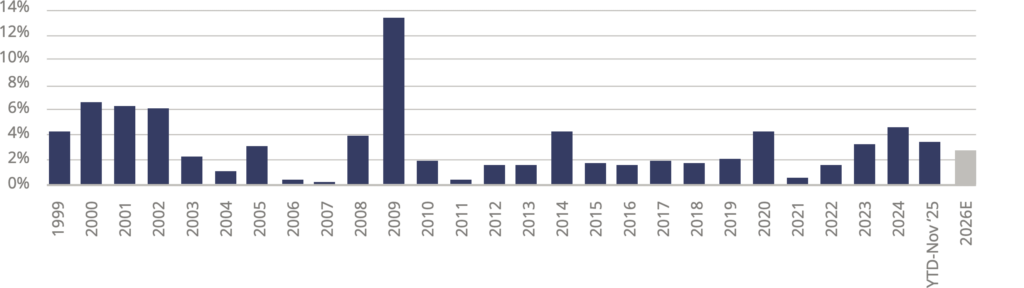

- We believe recent headline-grabbing, potentially fraud-related bankruptcies should not be viewed as a harbinger of a “cockroach” infestation of defaults for private credit. We expect leveraged loan and direct lending default rates to remain well contained in 2026 with credit coverage ratios continuing to improve.

- U.S. economic growth has exceeded expectations in 2025. Although areas of concern persist, economic growth prospects remain constructive for credit heading into 2026.

- Antares year-end 2025 survey of sponsors and borrowers suggest optimism for earnings growth and M&A activity. See survey here.

Direct lending return prospects remain favorable:

- Fed interest rate cuts are a headwind to floating rate yields but a positive for borrower stress relief and M&A volume growth trends which are expected to continue in 2026.

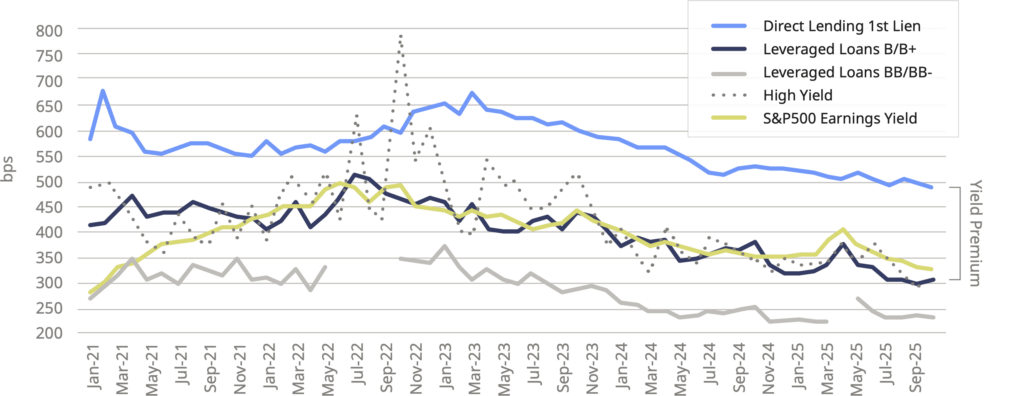

- Spreads have stabilized at lower levels across the credit spectrum, with direct lending’s yield premium vs. broadly syndicated loans holding up well.

- “Higher for longer” base rates in the forward SOFR curve suggest attractive long-term high single-digit unleveraged return prospects for direct lending.

- Direct lending’s natural inflation hedge remains an attractive attribute in the context of stimulative rate cuts and expanding government deficits.

Performance dispersion likely to remain elevated:

- Although borrower stress reflected in non-accruals and Payment In Kind (PIK) remains contained, dispersion among lenders has risen. Credit discipline, experience through cycles and strong workout capabilities remain critical areas of differentiation.

- We believe direct lenders with robust origination capabilities and sizable, established portfolios are best positioned to deploy capital efficiently, exercise selectivity, and achieve diversification—advantages that will be critical for distinguishing performance going forward.

AI is both threat and an opportunity:

- AI holds great potential to propel a renewed PE sponsor investment cycle aimed at creating value via productivity gains, revenue growth and new services and/or reshaped business models.

- From a private credit perspective, potential for business model disruption must be carefully evaluated via a disciplined framework that is responsive to rapidly evolving dynamics.

A Message from Timothy Lyne, Antares Capital CEO

Dear Investors and Partners,

We enter 2026 with a backdrop that remains strong for private credit, especially within direct lending, where conditions have improved meaningfully since the uncertainty that characterized the first half of 2025. Growth has proven resilient, inflation appears contained, and the Federal Reserve is expected to continue to ease interest rates. Together, these forces have contributed to spread stabilization, improving interest coverage and an uptick in deal activity, a trend we expect to continue.

At the same time, this is not a moment for complacency. As you will see in the report that follows, we are mindful of several factors. These include a reacceleration of inflation that could alter policy expectations, labor market deterioration that could challenge the resilience of growth, and a resurgence of trade or tariff uncertainty that could reprice risk quickly. We are also mindful of the early impact of AI on the broader universe of borrowers. As you will read in our report, the potential impacts are not balanced. We believe complex, mission-critical software platforms remain highly defensible, while other parts of the market that rely on lower switching costs or more traditional workflows may face greater pressure. The pace of change is rapid, and understanding these dynamics has become a critical part of assessing long-term credit quality.

As we look ahead, I find myself reflecting on the remarkable transformation of the private credit market. When Antares was founded 30 years ago, private credit was much smaller and far less defined with substantially fewer specialized lenders. The breadth of institutional and global participation we see today is greater than anything we envisioned at the outset. What we did have at the start, and what remains true today, was a belief that disciplined underwriting, deep sponsor partnerships, and a focus on consistency through cycles could create long-term value for investors and shareholders.

The private credit landscape has evolved markedly since those early days. Markets are more global, new segments have emerged, competition has grown, innovation has accelerated, and investor expectations have advanced. Yet one thing has remained constant for us – the discipline, selectivity, and hands-on approach that have defined our partnerships from the beginning, especially our deep and enduring sponsor relationships. Many of these partnerships date back to the earliest days of the firms we work with and the strength of those relationships, along with the depth of our existing portfolio, is central to how we remain highly selective insourcing compelling investment opportunities that align with our investment approach.

Equally important is how we underwrite and manage risk. Our approach has not wavered – we stay close to the companies we support, understand performance trends early, and engage proactively with sponsors when challenges arise. We integrate the insights of our underwriting, portfolio management, and credit advisory teams so we can identify potential issues before they compound and work collaboratively on solutions. This discipline, applied consistently across cycles, is central to how we protect capital and support long-term value creation.

We also see clear opportunity emerging. Investors are looking for more ways to stay invested in the asset class while accessing liquidity, and the market is responding. We are seeing momentum in areas such as the credit secondaries market and evergreen funds that offer flexibility and support efficient deployment. These developments reflect something important. Even as the industry changes, private credit continues to broaden, mature, and demonstrate its value across cycles.

As we approach 2026, and as Antares prepares to celebrate its 30th anniversary, I am reminded that longevity in our business comes from being consistent and earning trust. For three decades, we have stayed true to the disciplines on which we were founded, while expanding thoughtfully into new markets, new strategies, and new ways of creating value.

That disciplined approach positions us well for the environment ahead. We enter this next phase with appreciation, clarity, momentum, and a deep bench of talent committed to delivering value for you, our partners.

Thank you for the confidence you place in the Antares team.

Timothy G. Lyne

Chief Executive Officer

Looking back – Another solid year for Direct Lending

Reflections on 2025 and the set up for 2026 and beyond

In our 2025 outlook report, we anticipated “higher for longer” interest rates, heightened volatility and rising M&A activity with the potential for a surge. We also suggested that Wall Street earnings growth estimates for the S&P 500 were likely too optimistic but that growth would still prove constructive for credit. Finally, we predicted that prospects were favorable for direct lending returns, but that performance dispersion among lenders would remain elevated.

In the event, our prognostications were mostly correct, though some were a bit off the mark

- The Fed did hold rates flat through mid-September but ended up cutting three times through year end vs. our expectation of 1-2 cuts;

- There certainly was “heightened volatility associated with new administration policy” but we did not anticipate the magnitude of “Liberation Day” tariff shock to the markets and its dampening impact on M&A activity;

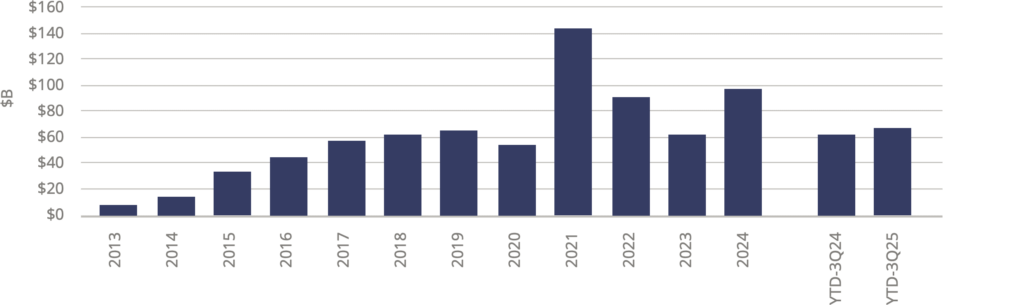

- Sponsored M&A related private deal volume did rise modestly YTD-3Q25 (see Exhibit 1), however, the recovery was less than expected;

- S&P 500 earnings growth forecasts for 2025 did come down from estimates of 14% at the beginning of 2025 to about 11-12% today, but we did not anticipate continued multiple expansion and an 18% total return for S&P 5002.

- Direct lending performed well in the YTD-3Q25 period as expected, with the Cliffwater Direct Lending Index (CDLI) on pace YTD-3Q25 to deliver an unleveraged return of about 9% in 20252.

Looking forward – Steady, as she goes

As we head into the new year, the press narrative around private credit has been decidedly downbeat with talk of credit problem “cockroaches” and repeated warnings of systemic risk brewing as private credit continues to grow.

Although there will always be select instances of fraud or default for the press to fret over, as we see it, the real big picture for private credit is likely to be largely a resilient (if mundane) “more of the same” story. Indeed, the Cliffwater Direct Lending Index (CDLI) total returns have continued to drone on in 2025 at a steady ~2-3% per quarter rate as they have since COVID, with the exception of 2Q22 when they dipped to just 0.5% following Russia’s invasion of Ukraine, a related spike in oil/inflation, and worries of an ensuing recession that never materialized.

Exhibit 1: M&A Volume Up Less Than Expected YTD But Believed to Be on Course for Further Improvement1

U.S. Direct Lending M&A Related Volume for Companies with $20-$120M of EBITDA

As we look forward, many of the same market themes we called out in 2025 remain at play heading into 2026. For example:

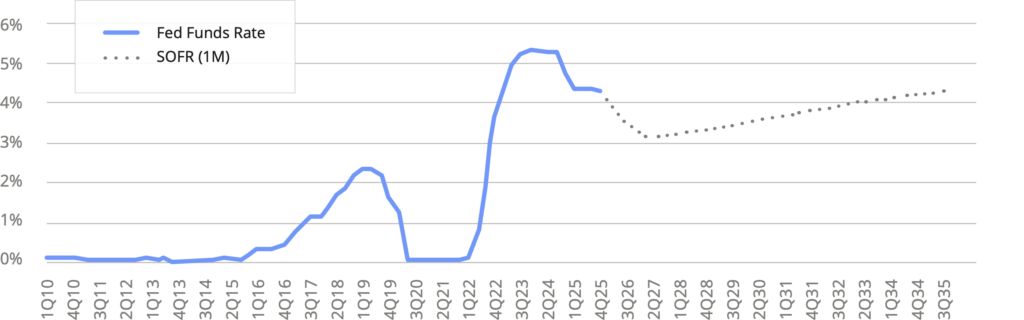

- The SOFR curve as of mid-December 2025 bottoms near 3% in late 2026 vs closer to a 4% target in late 2026 forecast in the curve at the beginning of 2025; however, base rates are still expected to remain “higher for longer” relative to the near zero rate environment of most of the last 15 years and the SOFR curve shows rates creeping back upward toward 4% beginning in 2027 (See Exhibit 2). The “higher for longer” SOFR curve suggests continued attractive long-term absolute direct lending return prospects.

- We anticipate lower financial market volatility in 2026 than seen in early 2025 following “Liberation Day.” However, there are sources of unsettling developments that could flare up across the spectrum of war/geopolitical risk, trade, and domestic politics. Also, Fed policy uncertainty or error leading to recession or a rekindling of inflation and/or a significant “AI bubble” market correction are also possible sources of volatility. Direct lending can provide an important source of ballast in portfolios during periods of volatility and tends to see increased opportunities when banks become more risk adverse in the syndicated market.

- The trend in sponsored M&A investment recovery is expected to continue and pick up pace into 2027 driven by lower interest rates, earnings growth, and continued pressure to return capital to investors (See Exhibit 1). Our recent year-end sponsor/borrower survey also indicates increased optimism for rising M&A heading into 2026. Increased M&A activity should lead to an increase in attractive “new money” opportunities to deploy capital.

Exhibit 2: Still “Higher for Longer” SOFR Base Rates Support Favorable Absolute Direct Lending Return Prospects2

Quarterly Average Fed Funds Rate and 3M SOFR forward Curve

Exhibit 3: Leverage Loan Default Rates Forecast to Decline in 20263

U.S. Leverage Loan Default Rate

- Although spreads have compressed across the credit spectrum, direct lending’s attractive yield premium remains robust (see Exhibit 4).

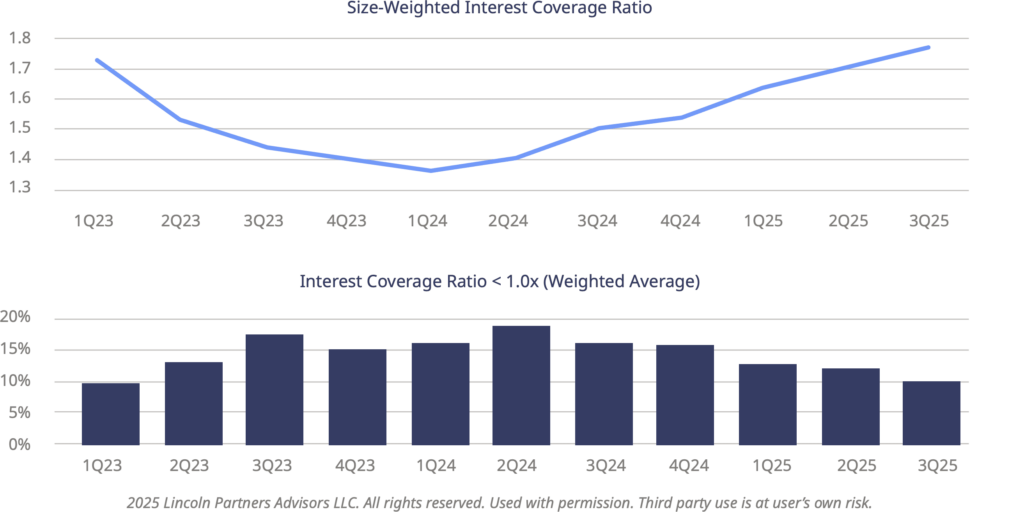

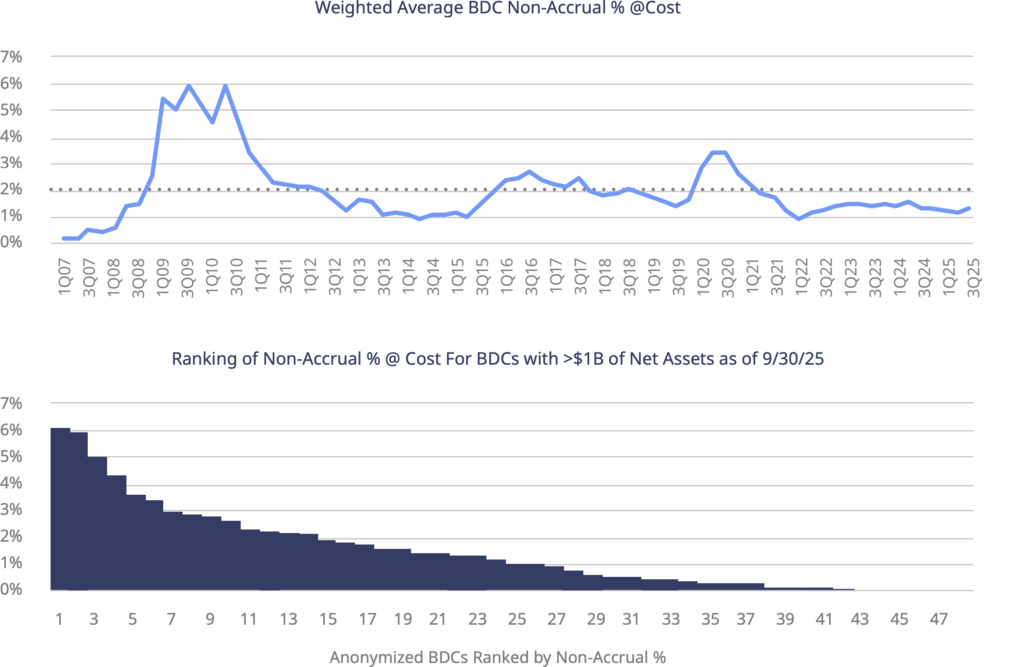

- The U.S. economy remains resilient with continued favorable earnings growth prospects. As was the case in early 2025, the currently robust 2026 bottoms up S&P 500 EPS growth forecast of 14%2 looks aggressive to us, but even less aggressive growth should prove constructive for credit as was the case in 2025. Credit metrics such as interest coverage are expected to continue to improve (see Exhibit 5), and non-accruals on average are expected to remain contained (see Exhibit 6).

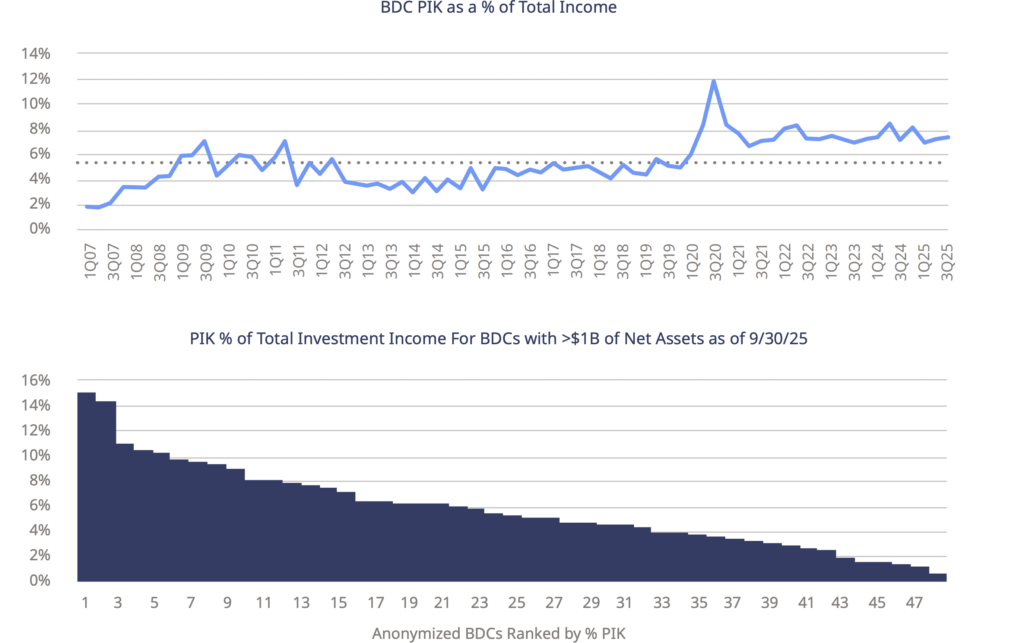

- We believe for the industry as a whole and for well-positioned, disciplined direct lenders in particular, the outlook “story” remains one of creating reliable value for both borrowers and investors. Of course, pockets of credit-stress still loom in select segments/vintages, spreads are compressed and AI could prove disruptive for some credits (topics to be discussed among others in the Q&A on page 12). No doubt, performance dispersion among lenders as evidenced in nonaccrual and PIK % of income is likely to remain elevated (see Exhibits 6–7).

Exhibit 4: Spread Compression Everywhere, But Direct Lending Yield Premium Remains Robust4

New Issue Spreads

Exhibit 5: Private Market Interest Coverage Ratios Improving; a Shrinking but Still Significant % Remain Stressed5

Exhibit 6: Weighted Average Non-Accruals Remain Tame, but Significant Dispersion Among BDCs6

Exhibit 7: PIK Levels Modestly Elevated vs Long-Term Average but Not Alarming; Dispersion Among BDC Significant7

Q&A with Edwin Cass, CIO of CPP Investments

We had the opportunity to speak with Ed Cass, Chief Investment Officer at CPP Investments, about his take on the U.S. macroeconomic environment and how his firm applies a Total Portfolio Approach in constructing a portfolio, the role of private credit, and how they deliver long-term returns for Canada Pension Plan’s beneficiaries and contributors.

Q1: What are your views on the U.S. economy the next few years? Given dollar debasement, is the U.S. still the “cleanest dirty shirt” among the top regions globally?

The global economy has broadly grown in line with its long-run potential, but U.S. growth has continued to exceed expectations. Consensus forecasts for 2025 and 2026 are now nearing two per cent. That’s half a percentage point higher than expectations a few months ago and essentially back to where consensus started the year. Consumer spending remains solid, even though the labor market is showing signs of softening.

A major source of that momentum stems from the ongoing AI-related investment cycle. This remains one of the most powerful forces shaping the U.S. economy today. Capital expenditure tied to AI has added meaningfully to growth this year, and forward-looking indicators point to further strength in both spending and revenues. We are still in the early stages of this cycle.

At the same time, inflation remains above the Fed’s target, with tariffs adding another layer of price pressure. While inflation has been more contained than many expected, some wholesalers appear to be absorbing tariff costs. If that dynamic fades, we could see renewed upward pressure on prices.

When we widen the lens, the U.S. still compares favorably with other major economies against this backdrop, currency dynamics have also added complexity. The U.S. dollar has been uncharacteristically volatile this year. It’s unclear if recent movements are more reflective of shifting interest-rate differentials, capital flows and currency valuations rather than concerns about outright debasement.

When we widen the lens, the U.S. still compares favorably with other major economies. Europe’s growth expectations have improved but remain structurally weaker due to demographic and productivity constraints. China continues to face excess capacity and persistent disinflation. Taken together, the U.S. benefits from the ongoing AI boom and corporate profits that are growing at a faster pace than in other developed and emerging markets.

Q2: CAIA recently published a paper in collaboration with CPP Investments on a “Total Portfolio Approach” to investing. Can you describe how the TPA works and its implications for private credit?

Before we talk about our Total Portfolio Approach, it’s worth mentioning that a key source of edge for us is the broad global capability we’ve built across many types of investments. Few investors combine a direct credit platform with the scale of one of the world’s largest private equity fund programs and one of the world’s largest real-assets platforms — all within one fund.

This capability is underpinned by our strategic move to a Total Portfolio Approach (“TPA”) in 2006 to strengthen long-term risk-adjusted returns and ensure the financial sustainability of the Fund. Rather than managing capital within individual asset class silos, we optimize as one portfolio for the right total fund exposures. At the heart of TPA is a focus on the underlying macro factors that drive value, which gives us a clearer picture of how the Fund will behave across a wide range of economic environments.

Within this framework, private credit is evaluated based on its overall contribution to the total portfolio, rather than in isolation. Our portfolio construction approach selects optimal market segments, ratings, maturities, and geographies across both public and private assets, ensuring the credit exposure we take aligns with the total portfolio’s risk-return objectives.

Instead of seeking credit beta—which can be replicated through public equity and fixed income—we aim for added value through thoughtful credit selection, which can lead to lower default rates.

Our scale and flexibility also allow us to invest selectively throughout the market cycle. As one of the largest direct private credit investors in the world, we have benefited from the structural advantages of the private credit investments spectrum — inflation hedging by investing in floating interest rate investments and preferential positions in the capital structure — generating attractive returns despite spread compression seen over the past two years.

As one of the largest direct private credit investors in the world, we have benefited from the structural advantages private credit offers such as an inflation hedge by investing in floating interest rate investments, preferential position in the capital structure, and an ability to generate attractive returns despite spread compression seen over the past two years

Credit investing requires disciplined, thoughtful execution, and sound judgement. We invest both directly in private credit as well as in building relationships with select managers who are aligned with our approach in areas where we see compelling scale and alpha generative opportunities. Our ownership of, and partnership with, Antares is an excellent example – and a differentiator that supports consistent long-term performance in an asset class that requires specific expertise.

Q3: How would you handicap the prospects for a productivity-driven Goldilocks scenario where we see high growth but also low inflation, versus an AI bubble that bursts? And what are the implications for credit?

Our objective is to construct a portfolio that remains resilient under various scenarios and one that delivers long-term returns for Canada Pension Plan’s contributors and beneficiaries, which underscores our emphasis on diversification.

Rather than predicting the likelihood of one outcome over another, our focus is on building a portfolio that can create alpha and be resilient in any market condition.

AI is playing an increasingly important role in today’s debate. It holds great potential to drive meaningful productivity gains and reshape business models, but it also brings real risks both on a macro level and at the individual credit selection level.

We believe the AI investment thesis can persist as technology drives structural changes in the economy and labour market. What remains uncertain is the pace of adoption and which companies will successfully pivot to take advantage of it.

In credit investing, where the asymmetry of returns limits upside opportunities relative to downside risks, loss avoidance is paramount. It’s why comprehensive, systematic evaluations of AI exposure and business risks across sectors and borrowers are critical in due diligence.

For long-term lenders with the ability to be selective and patient, the combination of AI-driven gains and occasional repricing episodes can create attractive opportunities. The key will be distinguishing between companies who are the true fundamental innovative beneficiaries of AI, and those who are just riding the wave.

AI holds great potential to drive meaningful productivity gains and reshape business models, but it also brings real risks both on a macro level and at the individual credit selection level.

Antares Capital Q&A Roundtable

How will the private credit markets fare in 2026? We sat down with four leading voices within the firm to discuss the outlook for deals, pricing, competition, and key risks worth keeping an eye on in the year ahead.

Q: How did 2025 shape up for private credit opportunities relative to expectations?

Shannon Fritz: There was a lot of optimism coming into the year, somewhat offset by geopolitical pressures, tariffs, rates, and the government shutdown. Notwithstanding those macro issues, direct lending continues to expand.

Tyler Lindblad: I second that. The direct lending market has been very resilient. We expected the M&A market would have been more robust, but it’s starting to pick up again.

Q: What evidence do you have of that?

Doug Cannaliato: Our pipeline of staples, which is what we call the financing packages we put together for our portfolio companies that are going to be for sale soon, has been growing throughout the year. In addition, our pipeline on a rolling 53-week basis has been on an uptrend since bottoming in early 2025. Both metrics don’t indicate gangbuster levels of activity, but they do suggest a higher level into 1Q26 and that’s expected to continue as the year progresses.

Q: How has the uncertainty impacted your ability to deploy investor capital?

Shannon Fritz: We’ve continued to deploy investor capital on a solid basis. Typically over 70% of our direct loans come from the roughly 500 companies across our portfolios, and incremental activity and refinance and recap activity have remained strong. Continued interest rate reductions should only help with that. And if we’re talking about uncertainty as it relates to the tariffs, our bottoms-up analysis shows a very limited direct impact. Our largest sectors are healthcare, financial services, business services and software, which are all mostly immune to tariff exposure.

Steve Rubinstein: We remain cautious on meaningful allocations to highly cyclical companies. We lend mostly to North American businesses that have a long-term history managing through multiple market cycles. Despite our robust diligence process and conviction in the businesses we lend to, we don’t need to make outsized investments in any single asset to ensure deployment in our funds. We continue to take advantage of the investment made in our private credit origination team that helps ensure we get the desired allocations to the best deals. That’s critical to our success.

Q: How are your portfolios performing heading into 2026?

Doug Cannaliato: Overall the performance is strong. On average the revenue and EBITDA are growing at a high single-digit rate, year over year. That’s across a diverse set of middle market borrowers. Add in increasing deal flow and expanding purchase price multiples, and it all adds up to a pretty healthy environment.

Steve Rubinstein: Our Institutional funds continue to provide current and consistent income to our LPs. We entered the wealth channel and launched our first BDC in early 2024. The Antares BDC’s are performing well. We’ve mirrored the same investment and portfolio construction strategy we have used for our institutional clients for the last 30 years. We invest in first lien only loans with a highly diversified, sponsor-owned focus on the core middle market.

Q: It seems like we’ve been saying for years that private equity firms are under increasing pressure to return money to their investors. What’s the argument that 2026 will finally see that happen?

Doug Cannaliato: There are two parts to this. First, hold times for private-equity-backed companies across our portfolios have stretched to five years or longer. Every day that passes creates more pressure to preserve IRR’s and return capital to LP’s. Second, the generally improving performance of portfolio companies and the expansion in purchase-price multiples over the past couple of years have created a constructive environment for transactions.

Tyler Lindblad: I think we’ll see a bifurcated market. In healthcare, business services, financial services, and software, there’s meaningful revenue growth and multiples have held up as a result. In sectors that are more economically and consumer spending sensitive, valuations are coming down. Those are also probably areas where sponsors have tried to hold on to their businesses, hoping that interest rates would come down or that those businesses would improve their performance and grow into their multiples. The calls to return capital are getting louder and while we have seen an increase in minority sales and continuation vehicles, I think you’re going to see those companies in the market transact and start to free up in 2026.

Q: In the meantime, are sponsors continuing to support their portfolio companies?

Tyler Lindblad: Yes, and it’s why direct lending has been very resilient. Sponsors have continued to support their businesses in meaningful ways. PE equity contributions are high and loan-to-value ratios are low. Sponsors have a lot of skin in the game.

Q: How has Antares been impacted by increasing competition in private credit?

Tyler Lindblad: Yes, meaningful money has been raised and it continues to increase, and that’s pressuring some structures and pricing. Ultimately, the industry will mature and consolidation will continue. The larger managers that have competitive advantages in terms of long-term relationships with sponsors and large and diverse portfolios that generate deal activity are going to continue to enjoy competitive advantages.

Steve Rubinstein: The market is competitive. Private credit has a long track record of consistent and favorable returns with low losses, so it attracts a lot of interest. We are not going to change what we do, and we have maintained the disciplined approach we bring to every decision. We focus on investing in high-conviction industries with sponsors who have a track record of growth and consistent support for their businesses.

We are not looking for increased yield to mitigate credit risk. That’s never been the strategy because the probability of default for those deals will likely increase.

Q: What sets Antares apart in this increasingly crowded market?

Doug Cannaliato: We’ve been in this market for almost 30 years, and we’ve earned a reputation as a thoughtful, reliable partner. That means that when a company has a headwind, we listen. We try to come up with solutions where everyone in the capital structure, including ourselves and the private equity firm is part of the solution. We’ll try to bring the company through whatever the issue is. At the end of the day, when we get past that headwind, our sponsor clients often look back and remember that they were listened to and treated fairly.

We also have exceptional access to deal flows. We review a large funnel of transactions every year and we whittle it down to only about 4% of the new deals that we close. So when we identify a transaction early in the process that we’d like to add to our portfolios, we indicate strong conviction in our interest to our sponsor client.

As a long-term reliable partner, sponsors frequently steer deals to us because they want us to lead their deals. This dynamic meaningfully supports our ability to build diversified, high quality credit portfolios.

Steve Rubinstein: I completely agree. In addition to our sponsor relationships, we have direct access to the borrower management teams. This is an important differentiator for us because it gives us information outside of the standard quarterly financial statements. If we want to see organic results, pricing/volume/margin trends, customer-level trends, cohort analysis, etc, then we have the direct access to request it. We have over 110 professionals on our private credit diligence team that underwrite and monitor these investments, and they know how to dig in when needed.

Q: Have syndicated markets been taking share away from direct lenders?

Tyler Lindblad: Private equity sponsors prefer to deal with direct lenders. They prefer the flexibility, certainty, confidentiality and speed that they offer. Plus, they prefer dealing with partners that they’ve done a lot of deals with, so that if they need to do add-on acquisitions, there’s flexibility, or if they have to restructure, they have long-term relationship lenders at the table. But they are only willing to pay so much of a premium for that. Sponsor behavior will continue to be driven by the pricing gap between the BSL market execution and the direct lending execution.

Doug Cannaliato: What’s unique about Antares is that we offer our sponsor clients private credit solutions and have full syndication capabilities to execute broadly syndicated loans.

We’re neutral about what solution is selected. We simply want to provide the solution that our sponsor client’s specific transaction needs. Increasingly, sponsors are choosing private credit because they’re not making financing cost their top priority. They’re more focused on certainty of terms, speed of execution and having a smaller lender group for future capital raises or any amendments that may arise.

Q: Is the feeding frenzy in private credit leading to lower underwriting standards? There have been some headlines this year that suggest cracks are starting to emerge.

Shannon Fritz: Some of the press around recent alleged fraud-related bankruptcies seem to try and make direct lending out to be the villain – but these were isolated situations that involved non-sponsored broadly syndicated loans and asset-based financing. They weren’t really direct loans. In sponsor-backed direct lending you have very thorough due diligence that is done up front by both the sponsor – which is sort of a first line of defense – and then of course by the lenders. Underwriting skill and experience varies among lenders and mistakes and fraud can happen, so LPs need to do their homework. But we don’t perceive there to be widespread systemic issues.

For our part, we don’t underwrite loans just to distribute them as banks do. We hold very significant portions of our loans as investments for our investors and our parent/owner CPP. Performing thorough due diligence and carefully monitoring credits remains as critical to our success as ever.

Q: How would we know if there were mounting credit issues in direct lending?

Shannon Fritz: There are a number of metrics analysts track, such as non-accruals, percentage of marks below 80 or 90, coverage ratios, risk ratings and payment-in-kind (PIK) levels. The large majority of are performing well against these stress metrics and we have been seeing some improvement. The credit issues that are out there now are mostly idiosyncratic or holdovers from the COVID era. Some of the deals done in the 2021 and 2022 vintages are facing challenges because they were done before interest rates shot up. Some may have had significant expansionary tailwinds coming out of COVID that caused improvement in the companies’ revenues and EBITDA that has proven unsustainable. Add to this inflation, tariff uncertainty and supply chain and other issues in certain segments and you have a challenging environment for underperforming companies to rebound and to exit.

Steve Rubinstein: Some chatter in the financial media suggests distribution yields coming down may be a leading indicator of stress – but that isn’t always accurate. These are mostly, if not entirely, floating rate assets. When the base rate declines, of course the net income for the BDC’s will decline and the distribution yield will also decline. But that is not necessarily a sign of stress like it is with equity when a company is cutting its distribution yield because it can’t generate cash.

Q: What specific signs of stabilization are you seeing in your own portfolio?

Tyler Lindblad: We spoke about revenue and EBITDA growth, but I’ll double back to what Shannon said about PIK. That refers to companies that defer part of their quarterly interest payments for a period of time, which can be a sign of stress. PIK funding from our portfolio – which was already lower than our competitors on a percentage basis – is starting to come down. That’s true across the industry. In addition, liquidity as measured by the percentage of revolver draws relative to their commitments, is near all-time lows, which indicates that liquidity amongst the broader set of borrowers is healthy. Overall, we expect stabilization and modest improvement in 2026 as interest rates come down, M&A activity improves, and certain companies’ performances continue to stabilize toward more normalized levels.

Q: Switching gears a bit here, have you been surprised by the extent to which AI is impacting direct lending?

Tyler Lindblad: Absolutely. AI is coming faster than any of us thought. I see it occurring on two axes. The first is from a productivity perspective. At Antares, we’re using it to drive greater efficiency, access information quicker, and make faster decisions, for instance, by putting together outlines of credit memos.

The second part is how AI is impacting new business underwriting. We have our own proprietary framework for that at Antares and we’re working hard to figure out which businesses are going to be benefactors from AI, which are going to be AI-neutral, and which ones face a genuine threat to their business from it (see “Our AI Risk Frameworks”).

Q: What could happen in 2026 that wouldn’t surprise you?

Shannon Fritz: There are pockets of the economy that are very strong, but I think there is more stress underneath the surface. I don’t see a great risk of recession, but we could have lower GDP growth than in 2025. Markets – particularly the stock market – may be underpricing that risk today.

Doug Cannaliato: I’m more optimistic about the economy. 2025 started off slower than it finished, because of all the tariff noise and global macro risks. As a result, the consumer, private equity firms, and CEOs across industries adopted a more cautious posture – whether related to capital investment, hiring, inventory decisions, or overall strategic initiatives. Many of those headwinds have since eased rather than intensified, which is contributing to a more constructive outlook.

Our AI Risk Frameworks

Artificial intelligence is materially impacting certain software use cases, including customer support with AI-powered chatbots, software development with AI-powered vibe coding, and human-centric services to name a few. AI is also enhancing the workforce by improving speed and quality of output and powering new, valuable insights into complex data sets quickly and efficiently. As investors seek to parse the winners and losers in an AI-enabled world, some are calling it quits on valuable segments of our economy, assuming “all” are at risk of being materially disrupted or displaced. Enterprise software companies are among those getting a hard look, due to the assumption that AI has opened the field to new entrants and approaches.

At Antares, we know AI will be disruptive for some enterprise software vendors, but we also know that many companies will continue to benefit from enterprise software for complex, well-integrated use cases that deliver a solid return on investment. Enterprise software vendors have access to the same models that start-ups do and often have access to better data to train AI that start-ups don’t; they maintain the incumbent client relationships generating meaningful ROI; and they have developed valuable and complex workflows that make switching challenging.

How can we tell which enterprise software vendors are going to win and which will lose in an AI-enabled world? Through our proprietary, repeatable, AI risk frameworks that help us to safely invest in solid and defensible business models.

We’ve developed two such frameworks. The first is aimed squarely at software companies and was developed by our dedicated team of experienced software underwriters that meet on an ongoing basis to “level set” regarding where AI is and where it’s going. We review industry research, speak with third party experts, and collect intelligence from our portfolio of borrowers and deals we review. We use these valuable public and private inputs to maintain the pulse of the AI evolution and to continually evolve our 12-point AI risk evaluation framework. The framework is used by our software underwriters when analyzing opportunities in the software space. It helps us to assess the potential for displacement risk, pricing model risk, and to determine their overall staying power in an AI-enabled world.

Our second framework extends this approach to non-software companies. It leverages our software vertical’s knowledge of AI and ways AI can disrupt a market, but it does so through a non-software company lens: continuing our laser focus on displacement risk but deeply evaluating drivers of switching from multiple perspectives. The resulting 13-point non-software AI risk evaluation framework helps guide our experienced teams to identify risks, think deeply about them, and sift through the commoditized opportunities to find differentiated, high-quality companies.

If we find that we can’t mitigate the AI risks that we uncover through our disciplined and proprietary approach, our course is clear: we turn the deal down. We have also found that the frameworks give us extra confidence to proceed when an investment remains supportable after both rigorous underwriting and evaluation via our proprietary AI risk evaluation frameworks.

We have run our portfolio through our AI risk evaluation frameworks, and they confirmed the value of our nearly 30 years of experience investing in mission-critical market leaders with defensible differentiation and high barriers to switching; this approach has and will continue to be a successful strategy in an AI-enabled world.

Importantly, we are never “done”; we continue to challenge ourselves to remain on top of macro and micro risks, continuously evolve our frameworks to ensure we can continue to deliver solid, risk-adjusted returns for our investors.

Conclusion

As we approach our 30th founding anniversary, we believe the market outlook for private credit and direct lending in particular looks favorable for 2026 and beyond. Although performance dispersion among lenders may widen, we believe our deep underwriting and dedicated workout experience through the decades, unique investor alignment, long tenured and deep relationships, sizable portfolio generating incumbent deal flow, and highly selective but broad origination and execution capabilities position us well to continue to deliver compellingly attractive risk-adjusted returns.

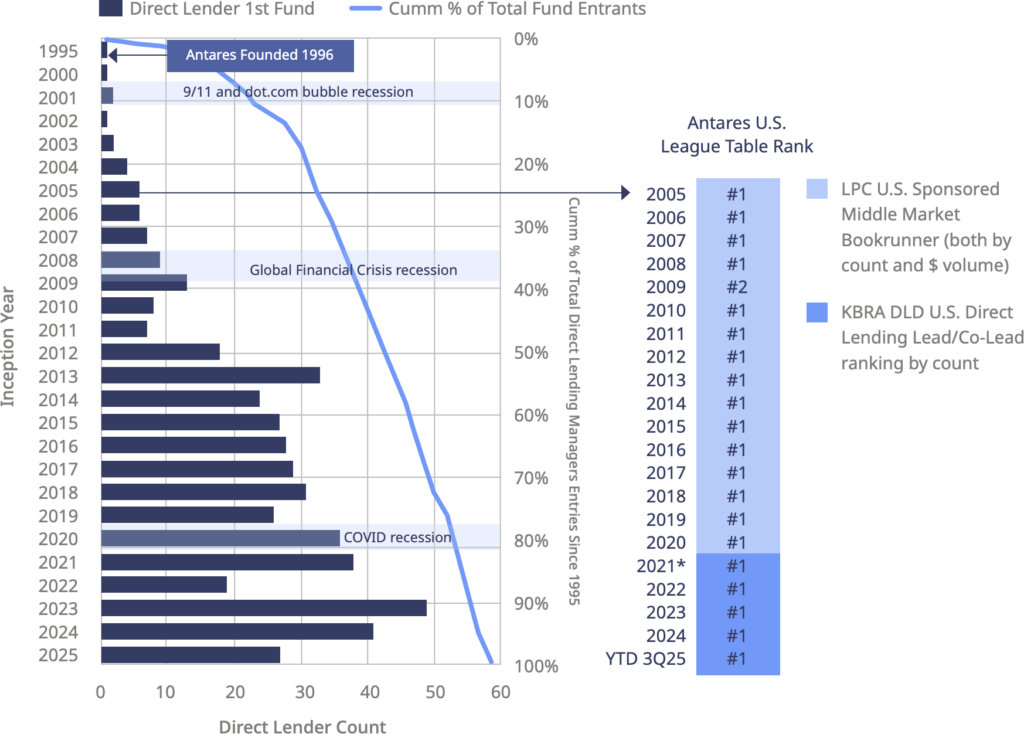

Exhibit 8: Few Direct Lenders Have Weathered Multiple Cycles with Most Entering Post the Global Financial Crisis*8

North America Focused Direct Lending Fund Manager Count by 1st Fund Inception Year

Exhibit 9: Antares Average Annual Loss Rate (2007-2024)9

Exhibit sources and notes:

- LSEG LPC Loan connector Direct Lending Module through 3Q25.

- Federal Reserve Economic Data (FRED) for Fed Funds Rate; Chatham Financial for forward SOFR curve as of Dec 10th, 2025.

- JP Morgan Leverage Loan Default Rate as of Nov. 30th, 2025.

- Cliffwater Direct Lending Index site for Direct Lending 1st Lien spread; Pitchbook LCD for Leveraged Loan and High Yield spreads, multpl.com for S&P 500 earnings yield – all through October 2025.

- 2025 Lincoln Partners Advisors LLC. All rights reserved. Used with permission. Third party use is at user’s own risk.”Source: Lincoln International’s Lincoln Lens database as of 3Q25.

- Cliffwater Direct Lending Index site for Weighted Average BDC Non-Accrual % @Cost as of 3Q25; LSEG LPC BDC Collateral database for Ranking of Non-Accrual % @ Cost For BCDs with >$1B of Net Assets as of 9/30/25.

- Source: Cliffwater Direct Lending Index site for BDC PIK as a % of Total Income as of 3Q25; LSEG LPC BDC Collateral database for Ranking of Non-Accrual % @ Cost For BCDs with >$1B of Net Assets as of 9/30/25 (Note includes all BDCs with 3Q25 reported data as of Dec. 8th 2025).

- North American focused direct lending fund manager count by inception year from Preqin’s fundraising database as of September 15, 2025. LSEG LPC U.S. Sponsored middle market bookrunner league table ranking by both count and $volume from 2005-2020 and then switch as shown in Exhibit to KBRA Direct Lending Deals (DLD) Direct Lender ranking by count shown for 2021-1H25. KBRA DLD first published its direct lending rankings in 2021, and we switch to showing this ranking as of when it became available because it is more representative in covering the market Antares serves with direct lending having gained share from the syndicated market over the years, with dominant share now in the middle market.

- Antares Loss Rate: “Loss Rate” is the quotient of (i) cumulative Realized Losses divided by (ii) cumulative Invested Capital, annualized by dividing such result by the number of years since 2007, as of the reporting period. Note: Loss performance pertains only to Antares Core Business Loans and Private Credit Composite Loans; Gains or losses associated with investments other than such loan positions, including without limitation, equity investment in borrowers(or their affiliates) other than equity positions received as part of a debt-to-equity conversion, and unrealized loans, are excluded.

Footnotes:

1Cliffwater 2025 Q3 Report on U.S. Direct Lending, Dec 1st, 2025

2Source: FactSet Earnings Insight Dec. 5th, 2025

Disclosure for Marketing Brief and Marketing Research/Outlook

The materials presented herein are provided to you solely for informational purposes and unless otherwise indicated herein, has been prepared using, and is based on, information obtained by Antares Capital (“Antares”) from publicly available sources. It does not constitute an agreement, or an offer, commitment to offer, or agreement to sell any loans, securities or other assets including interests in any fund or vehicle. The materials contained herein are not intended, nor should they be construed or implied, to be a recommendation or advice of any kind. The information set forth herein has been compiled as of the date(s) noted, is preliminary and subject to change. There is no obligation on the part of Antares to update the information provided herein after the date hereof. Neither Antares nor any affiliate thereof represents or warrants the accuracy, completeness or reliability of any of the materials contained herein, either expressly or impliedly, for any particular purpose, and shall have no duty to update or correct any such information. Without in any way limiting the generality of the foregoing, you understand that certain of the information provided herein is based on information provided by third parties, and neither Antares nor any affiliate thereof makes any representation or warranty regarding the accuracy, completeness or reliability of any such information. In no event will Antares be liable for any losses or damages arising from or as a result of the use of the information or the materials contained herein. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Antares believes that such information is accurate and that the sources from which it has been obtained are reliable; however, none of Antares nor any of its affiliates or agents can guarantee the accuracy of such information and they have not independently verified and are not responsible for any inaccuracies, omissions and outdated information contained in such third-party information or the assumptions on which such information is based. Certain other information regarding market analysis and conclusions could be based on opinions or assumptions (including those of Antares) that Antares considers reasonable. Unless otherwise indicated, such market analysis and conclusions represent the subjective views or beliefs of Antares.The materials presented herein may include certain projections, forecasts and estimates that are forward-looking statements. Any such forward-looking statements are based on certain assumptions about future events and are subject to various risks and uncertainties. Forward looking statements are necessarily speculative in nature and it should be expected that some or all of the assumptions underlying them will not materialize or will vary significantly from actual results. Accordingly, actual results will vary from the projections, and such variations may be material. Some important factors that could cause actual results to differ materially from those in any forward-looking statements contained in these materials include, without limitation, changes in interest rates, default and recovery rates, market, financial or legal uncertainties, the timing of acquisitions of loans, the types of loans acquired, differences in the actual allocation of loans from those assumed mismatches between the time of accrual and receipt of interest proceeds from the loans and whether or not and how loan investments may be leveraged.Any statements involving matters of opinion or estimates, whether or not so expressly stated, are set forth as such and not as representations of fact, and no representation is made that such opinions or estimates will be realized. The statements and expressions of opinion contained in this presentation are subject to change without notice and involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon nor should they form the basis of an investment decision.