Introduction to Elements of Private Credit

A brief overview of private credit and why it has become a core part of modern capital markets.

A practical education platform to help advisors learn, assess, and monitor private credit.

Hear from our CEO

Watch An introduction to private credit, led by Antares founder and CEO, Timothy Lyne. · VideoAs private credit becomes a more established part of income-oriented portfolios, the focus for advisors is shifting from access to selection and implementation—understanding how to best assess, monitor, and explain exposure with clarity and discipline. This education platform is designed to help.

The Elements

Definitions

From foundational private credit concepts to advanced allocation strategies, our education platform supports advisors wherever they are in their private credit journey.

Learn

Direct lending, built for certainty and flexibility

Private credit includes a range of strategies, but direct lending is the largest and most relevant starting point for most advisors. It refers to privately negotiated loans made by a single lender or small group of lenders, typically to middle-market companies, often backed by private equity firms (sponsors).

Compared with traditional bank lending, private credit often provides greater speed, simplicity, flexibility, and customization—while offering investors contractual income and senior positioning in the capital structure.

Featured Content

A loan directly negotiated with a corporate issuer that is usually senior in the capital structure and secured by assets.

A loan typically originated by one or more banks and then sold to a wide pool of institutional investors. A complex process entailing roadshows and engagement with ratings agencies.

![A graphic explaining Syndicated Loan (BSL). The Lender (Large group of investors [“syndicate”]) gives the loan principle to the Borrower (Typically a very large corporation, often backed by private equity sponsor) through an Intermediary (a Bank). The Floating Rate Interest Payments/Transaction Fees go from the Borrower, through the Bank, to the Lender.](https://www.antares.com/wp-content/uploads/2026/05/borrower-bank-lender-graphic.svg)

Why private credit has grown

Private credit has developed over multiple decades as banks have reduced their role in middle-market lending. Regulatory change, balance-sheet constraints, and industry consolidation created space for non-bank lenders to provide capital, while institutional investors stepped in to help meet growing demand.

A lending gap emerges

Structural changes in the banking industry resulted in a multi-decade shift from traditional bank lending to private markets. A wave of bank consolidation beginning in the late 1990s reduced the availability of relationship-based lending. This retrenchment accelerated in the aftermath of the GFC, as banks further tightened underwriting standards and scaled back middle-market exposure.

The rise of private equity-backed lending

As banks became more risk-off and increasingly focused on larger borrowers after the GFC, many middle-market companies faced more limited access to debt financing. Non-bank lenders stepped in to help fill that gap. At the same time, the rapid growth of private equity increased demand for private market financing solutions. For firms like Antares, which has been active in sponsor-backed lending since 1996, this period marked both a major market shift and the acceleration of a model already taking shape.

The middle market opportunity

Despite the asset class’s growth, overall penetration remains relatively low, with private equity ownership still representing less than 15% of the middle market. More recently, interest rate volatility has also increased investor interest in higher-yielding fixed income alternatives, including private credit.

Private credit is typically used to provide contractual income with senior-secured positioning that may support downside protection. Compared with many public credit instruments, private loans may exhibit lower price volatility owing to the non-traded, buy-and-hold nature of the market, as well as asset-specific dynamics that can lead to more constructive solutions during periods of stress.

| Private Credit | Bank Loans | High Yield Bonds | |

|---|---|---|---|

| Commonly Known As | Direct Lending | BSL or Leveraged Lending | Non-Investment-Grade Bonds |

| Public vs. Private | Private | Public | Public |

| Seniority | Senior-Secured | Senior-Secured | Unsecured |

| Liquidity | Lower | Moderate | Higher |

| Coupon Rate | Floating | Floating | Fixed |

| Price Volatility | Lower | Moderate | Higher |

Within a diversified portfolio, private credit is often positioned alongside traditional fixed income to enhance income and provide differentiated exposure. As allocations to private credit grow, manager selection should also include asset-level look-through: when using multiple managers, limited overlap and complementary exposure can be important to achieving true diversification.

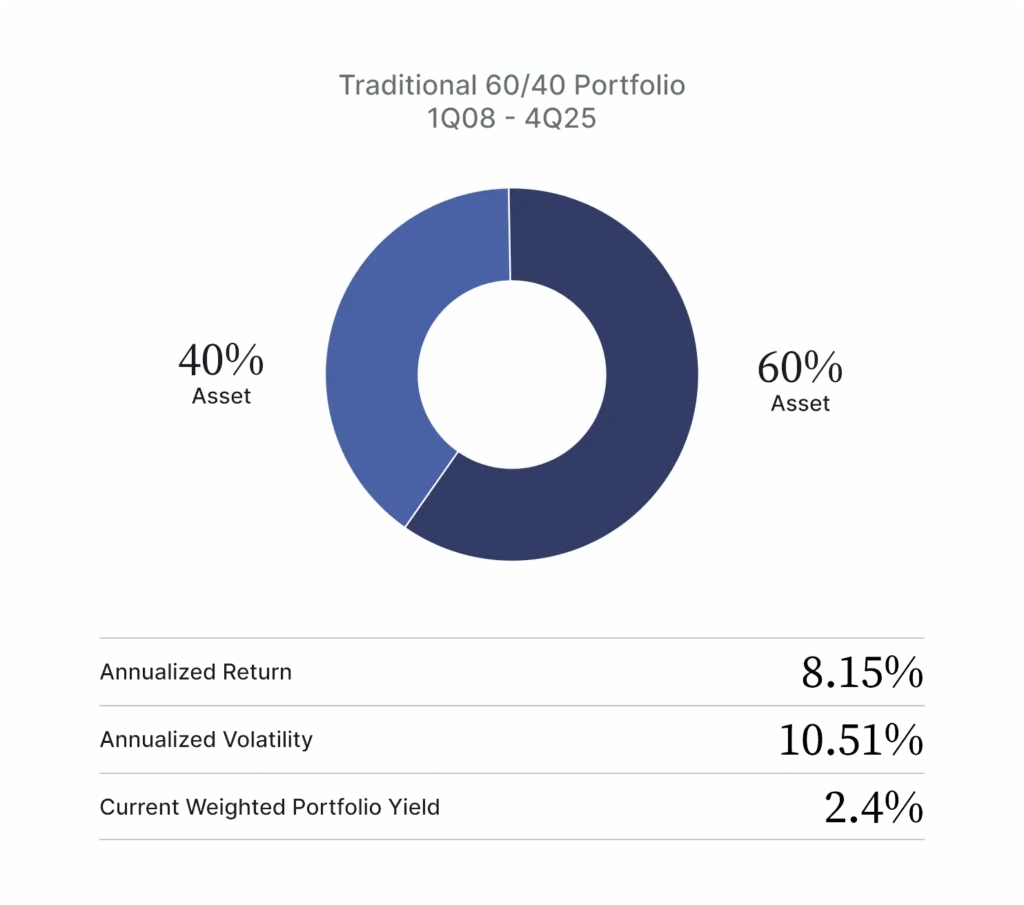

In a typical 60/40 portfolio, equities are the primary contributor to performance and volatility.

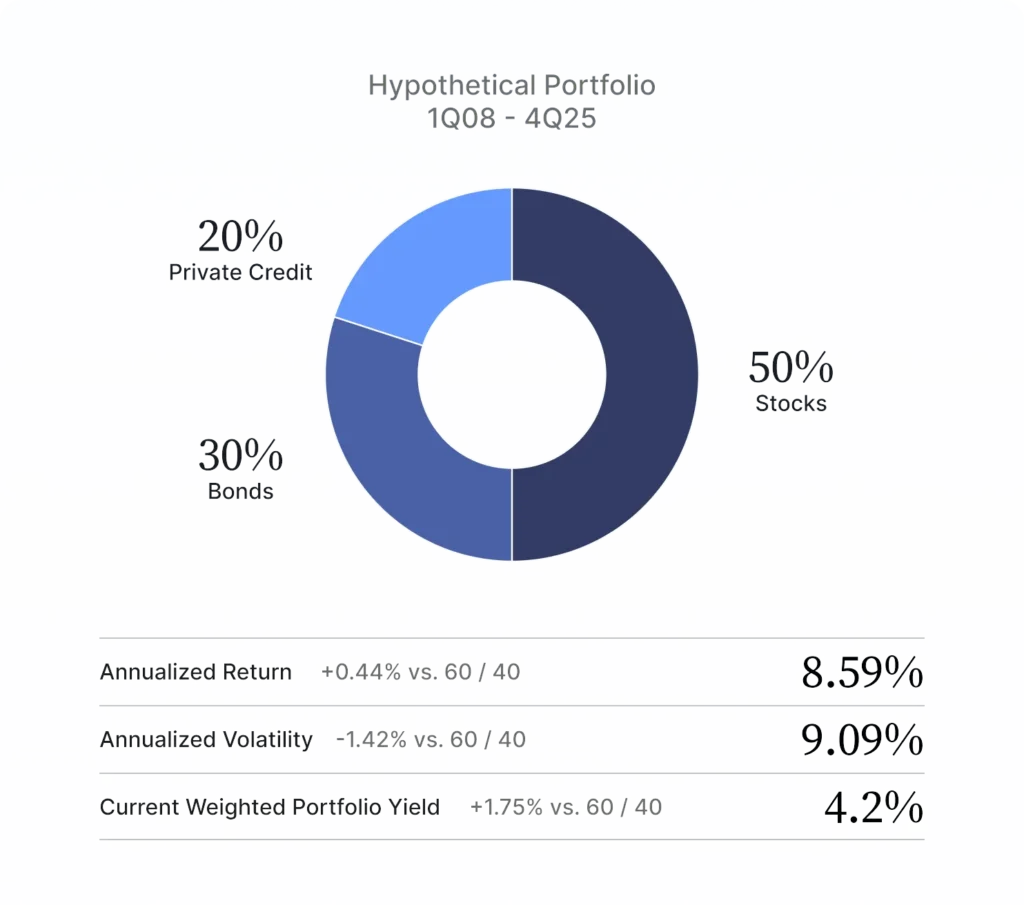

A hypothetical portfolio of 50% stocks, 30% bonds and 20% private credit results in higher returns, higher income and lower volatility.

Source: Cliffwater LLC and Bloomberg as of December 31, 2025. Note: Represents Antares’ beliefs. Past performance is not a reliable indicator of future performance and future results may differ materially. Benchmarks: Direct Loans = Cliffwater Direct Lending Index. The CDLI is an asset-weighted index by reported fair value of directly originated middle market loans which CLDI recognizes realized gains (losses) mostly in the form of realized losses generated by write-downs of loan principal that result from borrower default or restructuring. The CDLI rates shown above are calculated as the average of the annual Realized Credit Losses, as reported by Cliffwater. Bonds = Bloomberg Barclays U.S. Aggregate Bond Index. Stocks = S&P 500 Index. The information provided is for educational purposes only.

Direct lending typically involves privately negotiated loans to sponsor-backed middle market companies, structured through bilateral or small lender groups and held as long-term investments. Compared to broadly syndicated loans, this approach offers greater speed, flexibility, and certainty of execution—while enabling stronger alignment between borrowers and lenders over the life of the loan.

Yield Premium

Direct lending may offer a yield premium over broadly syndicated loans and high yield, reflecting its illiquid, privately negotiated nature—historically without higher loss rates.

Downside Protection

Senior secured positioning, conservative loan-to-value ratios, and strong covenants help protect capital, supported by sponsor backing and more constructive outcomes in stressed situations.

Floating-Rate Income

Floating-rate structures help preserve real income as rates rise while limiting duration risk, with contractual floors that may help stabilize yields when rates decline.

Lower Return Volatility

Contractual income, low duration, and a buy-and-hold investor base have historically contributed to more stable return profiles than many traded credit assets.

Diversification Benefits

Direct lending provides access to a broad universe of private, middle market companies not available in public markets as well as other portfolio diversification benefits.

Assess

A framework for advisor due diligence

The private credit BDC market has expanded rapidly, giving advisors a broader range of choices—and making manager selection more important. Evaluating a BDC today requires more than comparing headline yield. Portfolio construction, underwriting discipline, and early signs of credit stress can materially shape outcomes over time.

Advisors should look beyond surface-level metrics to understand how credit decisions are made, how risk is managed, and how portfolios are expected to perform across different market environments.

This framework highlights three areas that can help advisors assess BDCs more effectively. It provides a clearer view into how a strategy is built, where risk may emerge, and how outcomes may evolve over time.

For a deeper discussion of the specific questions, metrics, and signals to evaluate within each area, connect with the Antares Wealth Solutions team.

Evaluating private credit requires a clear framework that highlights the questions, indicators, and areas of differentiation beyond yield.

Talk to the Antares Wealth Solutions team to dive deeper into the framework.

Get in TouchThese three areas provide a practical way to assess how a BDC is constructed, managed, and positioned over time. Applying them effectively requires understanding the specific questions, metrics, and signals that can differentiate outcomes across managers and market environments.

Portfolio Quality & Risk:

Assess the underlying portfolio to understand how it is built, where risk is concentrated, and how it may behave across different market environments.

Manager Quality & Credit Capabilities:

Evaluate whether the manager has the scale, sourcing advantages, underwriting discipline, and experience to build and protect value over time.

Vehicle Structure & Investor Fit:

Assess how the vehicle’s structure, liquidity profile, and shareholder dynamics may shape client experience, portfolio behavior, and long-term suitability.

Monitor

Is the strategy delivering the income you expected?

Private credit is often used for contractual income, but because most loans are floating rate, income should be evaluated based on delivery over time, not a static headline yield. Base rates matter, but so do spread, floors, financing costs, leverage, non-accruals, PIK, repayments, and credit losses.

Base Rates Change

These can influence the level of income generated by floating-rate loans.

Base rates are only one driver of income. Income delivery also reflects spread, floors, financing costs, leverage, non-accruals, PIK, repayments, and credit losses.

Repayments

Early pay-downs can reduce income and require reinvestment at new market rates.

Payments in Kind (PIK)

Interest paid in additional principal rather than cash may indicate rising borrower stress.

Non-accrual Activity

Loans that stop generating interest income can signal credit deterioration.

Are borrower fundamentals or lender protections changing?

Monitoring credit quality is about identifying changes before they show up in returns. These indicators can help investors assess whether portfolio risk remains consistent with expectations.

Loan Documentation / Lender Protections

Documentation quality can shape monitoring, control, and recovery outcomes. Investors should pay attention to covenant structure, EBITDA definitions and add-backs, baskets, collateral protections, and other terms that influence lender rights.

Leverage / Attachment Point / Loan-to-Value

Leverage matters, but so does where the lender sits in the capital stack and how much enterprise value or collateral support sits beneath the loan. Together, these metrics can provide a clearer view of downside protection.

Amendment Activity

Amendments can be a useful signal when viewed in context. Higher amendment volume may indicate changing borrower conditions, weaker original underwriting, or greater lender accommodation. Additionally, an increase in PIK (payment-in-kind) interest within amendments may signal borrower stress or cash flow constraints, as interest is deferred rather than paid in cash.

Non-Accruals

Loans placed on non-accrual no longer contribute current income and may reflect underlying credit deterioration within the portfolio.

Does the portfolio still reflect its intended role?

Portfolio exposures can help determine whether a strategy remains aligned with its intended role in a broader allocation.

Seniority Mix

Where the portfolio sits in the capital stack is foundational. Greater exposure to senior secured loans may support stronger downside protection than portfolios with more junior debt or equity exposure.

Borrower Diversification

The number of borrowers and the size of each position matter. A more diversified portfolio may be better positioned to absorb idiosyncratic credit issues without outsized impact from any single name.

Borrower Size

Smaller companies may offer higher yields, but they can also carry greater operating risk and less resilience during periods of stress.

Sector Exposure

Concentration in certain industries can increase sensitivity to sector-specific downturns, regulatory shifts, or cyclical pressure.

Sponsor Concentration

Exposure to a limited number of sponsors can reduce diversification and increase dependence on a narrower set of underwriting relationships.

How does the manager respond when conditions change?

Private credit outcomes depend heavily on underwriting consistency, ongoing monitoring, and workout execution, particularly during periods of stress.

Featured Content

Documentation Discipline

Strong managers maintain discipline not only on pricing and leverage, but also on documentation quality. Covenant protections, collateral packages, and limits on leakage can materially affect outcomes.

Recoveries

Recovery outcomes after defaults or restructurings can provide insight into collateral protection, restructuring capabilities, and the manager’s ability to preserve value.

Realized Losses

Actual losses remain one of the clearest measures of whether underwriting, portfolio construction, and workout execution have held up over time.

Portfolio Monitoring and Intervention

A manager’s ability to identify issues early, stay close to borrowers, and act before problems become impairments can be as important as the original investment decision.

Speak with Antares Wealth Solutions to learn more about how to evaluate private credit.