Fed Rate Cutting Cycle Implications For Direct Lending Returns

Key Points:

- The Federal Reserve has restarted a rate cutting cycle after an 8 month pause.

- For direct lending investors, lower SOFR means lower yields, but it also means potentially healthier borrowers, more M&A activity, and lower cost of liabilities.

Bottom Line:

Lower base rates may trim near-term returns, yet history and today’s SOFR curve point to attractive risk-adjusted outcomes ahead. We believe direct lending’s income, credit protections, and relative premium are poised to remain intact over the cycle.

Implications of Lower Base Rates Not All Bad For Direct Lenders

On September 17th, the Federal Reserve cut the Fed Funds rate by 25 basis points as widely expected, with the most recent Fed “dot plot” suggesting a further slow descent ahead for the Fed Funds rate from just over 4% to just over 3% by early 2028. In contrast, the 3M term SOFR forward curve1 suggests a slightly faster pace of cuts, with SOFR bottoming at just below 3% by late 2026/early 2027 (as of Sept 17th).

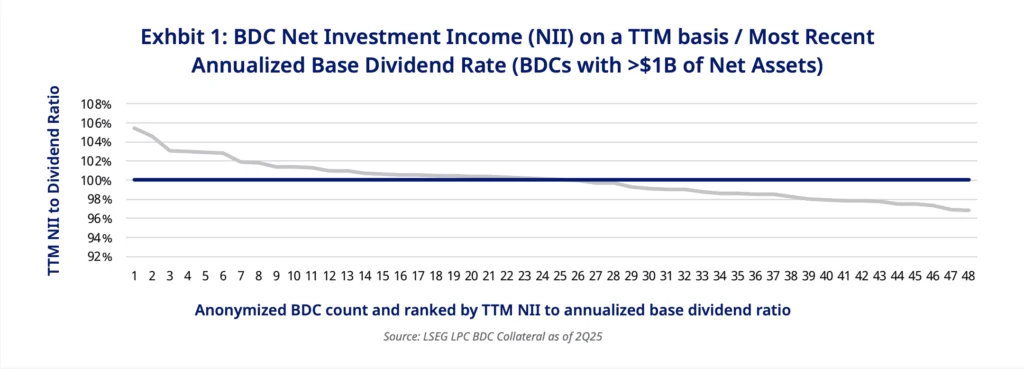

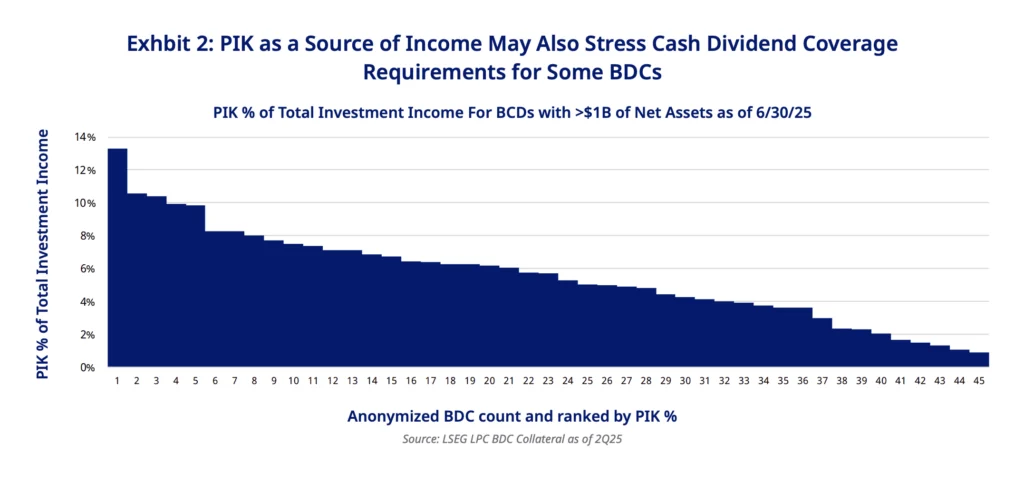

For floating rate loans, this expected ~1% drop in SOFR base rates is an obvious headwind to the absolute yield income component of returns, and will likely lead to cuts in supplemental and some base dividends for BDC’s – especially those with low or negative net investment income (NII) dividend coverage, high non-accruals and/or high levels of non-cash paying PIK. Some BDC’s have already cut their dividends.

Net Investment Income includes Payment-In-Kind (PIK) income (see Exhibit 2) which is non-cash, and this too bears on a BDC’s ability to cover its cash dividend payment requirements.

That said, a 1% drop in base rates is not particularly dramatic as far as interest rate cycles go and presumably not outside the bounds of most BDC boards’ planning assumptions. In addition, there are other offsetting positives that come with a 1% drop in base rates that can help offset lower yields on portfolio assets including:

- Lower cost of capital on floating rate liabilities as an offset to reduced interest revenue

- Ability to alter fund level leverage, subject to deployment opportunities

- Asset mix management (e.g. minimize lower yielding broadly syndicated loan holdings). Here, however, it’s important not to have too much style drift or to chase much higher risk assets

In addition, the market may help with:

- Increased M&A activity as rates fall

- Increased fees related to increased portfolio turnover

- Potentially lower loss rates as borrower interest cost burden falls

- Spread stabilization and possible widening depending on economic circumstance

How Has Direct Lending Performed in Prior Cycles?

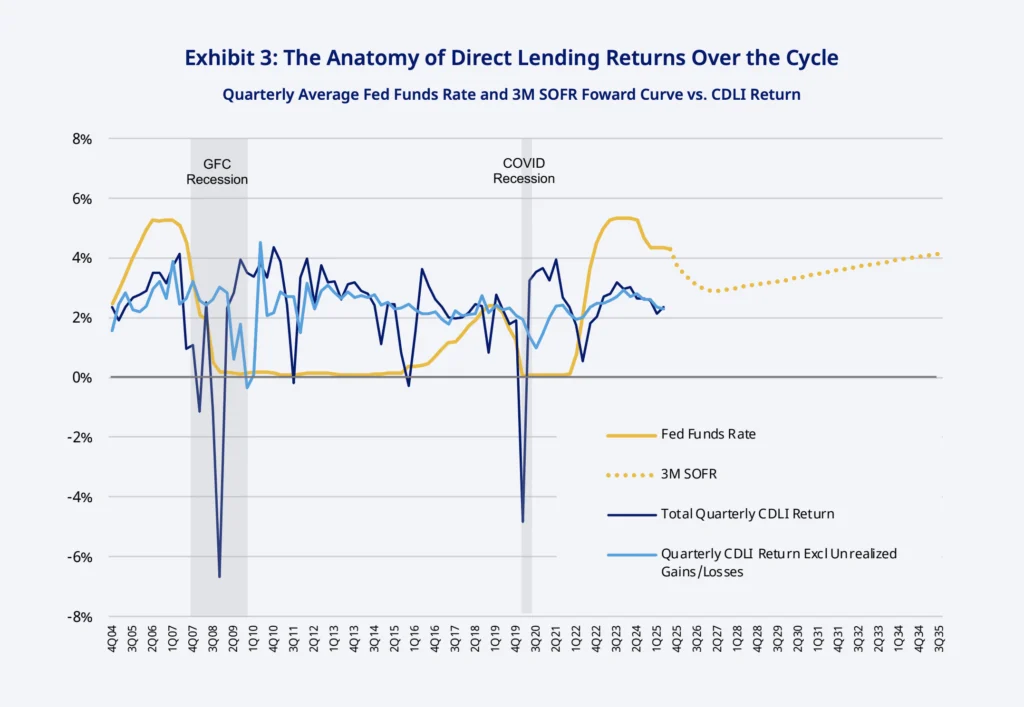

There have been two major historical Fed interest rate cutting cycles since the Cliffwater Direct Lending Index started in 2004, with the third currently underway as can be seen in Exhibit 3. However, the previous two rate cutting cycles were accompanied by recessions (Global Financial Crisis and Covid recessions), and base rates in both cases fell to near zero. The current cycle, in contrast, does not appear to be on the same course, with base rates expected to bottom near 3% before rising once again. Whether a recession is forthcoming is of course uncertain. Most economists forecast a slowdown but not a recession, and the Atlanta Fed’s GDPNow indicator currently points to a relatively healthy ~3% GDP growth rate in 3Q25.

That said, the odds of a recession in the next 12 months may have risen following a string of weak labor market statistics and a related recent fall in consumer confidence. If there is a recession forthcoming, it would no doubt weigh on direct lending return performance. As can be seen in Exhibit 3, the Cliffwater Direct Lending Index (CDLI) experienced a peak 6% quarterly drawdown in 4Q08 during the GFC recession and an almost 5% drawdown in 1Q20 at the start of COVID. Here, however, it is important to bear two things in mind:

- The peak CDLI quarterly drawdowns were modest relative to other asset classes like leveraged loans, high yield bonds, and stocks during these recessionary periods and;

- The CDLI drawdowns during the GFC and COVID recessions were primarily associated with unrealized losses which either turn into realized losses or cancel out over time. If one excludes the unrealized loss component of the CDLI’s returns and just looks at the realized gains/losses and income components of the CDLI’s returns since 2004 (blue line in Exhibit 3), the only negative return quarter over the period was -0.34% in 4Q09 when enough unrealized losses in the previous quarters were converted to realized losses to offset the income component of return.

Long Term Risk Adjusted Return Prospects Remain Favorable

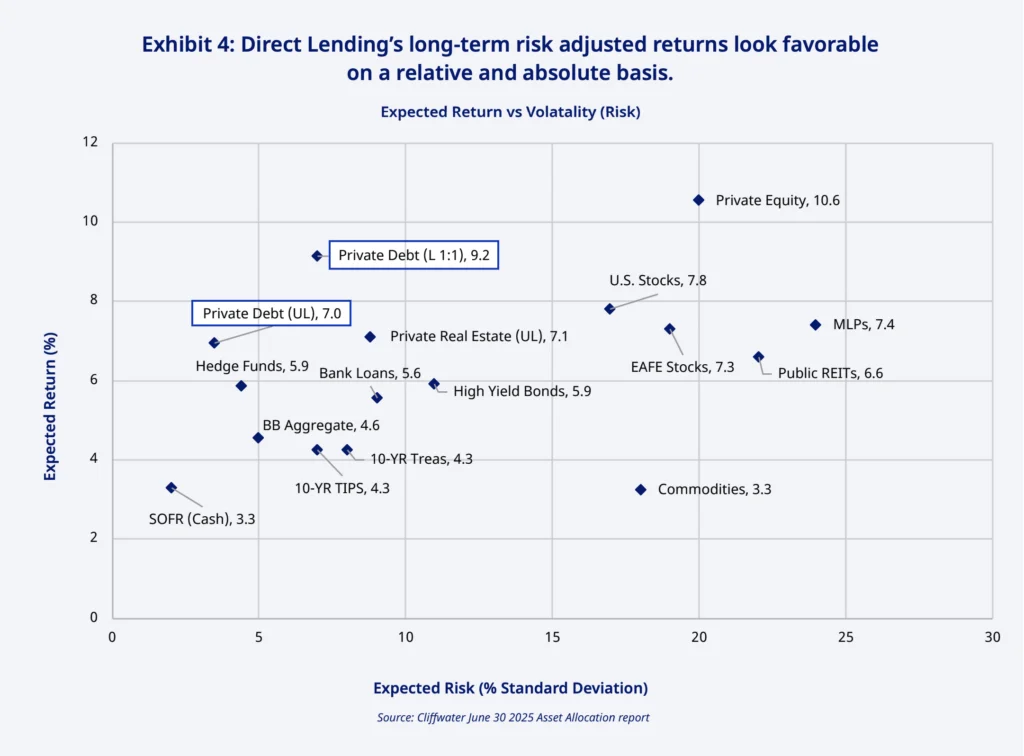

As can be seen in Exhibit 3, the most recent SOFR curve continues to point to “higher for longer” base rates in the future vs. most of the past 2 decades. Granted an average 3.3% SOFR rate over the next 10 years, Cliffwater LLC continues to show an attractive expected risk/return profile for direct lending (shown as “Private Debt” in Exhibit 4) on both an absolute basis and relative to most other asset classes (see Exhibit 4).

When a recession will arrive is hard to forecast, but one will come at some point. When it does, direct loan performance is expected to be resilient, particularly for managers with disciplined credit selection, experience through multiple cycles and deep workout capabilities. Should a typical recession case scenario transpire in the year ahead, Cliffwater analysis suggests three-year annualized returns could recover to 7.8% for the CDLI.2

Footnotes:

1 Source: Chatham Financial as of Sept 17th, 2025

2 Source: Tariffs, Recession, and Downside in Private Debt, April 14, 2025; Cliffwater LLC. Note: Cliffwater estimates three-year annualized recession-scenario returns to be 6.2% for BDCs and drawdown funds (on average) after fees reflecting use of leverage.

Disclosures

The materials presented herein are provided to you solely for informational purposes and unless otherwise indicated herein, has been prepared using, and is based on, information obtained by Antares Capital (“Antares”) from publicly available sources. Information provided herein is subject to change depending on market conditions. It does not constitute an agreement, or an offer, commitment to offer, or agreement to sell any loans, securities or other assets including interests in any fund or vehicle.

The materials contained herein are not intended, nor should they be construed or implied, to be a recommendation or advice of any kind. The information set forth herein has been compiled as of the date(s) noted, is preliminary and subject to change. There is no obligation on the part of Antares to update the information provided herein after the date hereof. Neither Antares nor any affiliate thereof represents or warrants the accuracy, completeness or reliability of any of the materials contained herein, either expressly or impliedly, for any particular purpose, and shall have no duty to update or correct any such information. Without in any way limiting the generality of the foregoing, you understand that certain of the information provided herein is based on information provided by third parties, and neither Antares nor any affiliate thereof makes any representation or warranty regarding the accuracy, completeness or reliability of any such information. In no event will Antares be liable for any losses or damages arising from or as a result of the use of the information or the materials contained herein.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources.

Antares believes that such information is accurate and that the sources from which it has been obtained are reliable; however, none of Antares nor any of its affiliates or agents can guarantee the accuracy of such information and they have not independently verified and are not responsible for any inaccuracies, omissions and outdated information contained in such third-party information or the assumptions on which such information is based. Certain other information regarding market analysis and conclusions could be based on opinions or assumptions (including those of Antares) that Antares considers reasonable. Unless otherwise indicated, such market analysis and conclusions represent the subjective views or beliefs of Antares.

The materials presented herein may include certain projections, forecasts and estimates that are forward-looking statements. Any such forward-looking statements are based on certain assumptions about future events and are subject to various risks and uncertainties. Forward-looking statements are necessarily speculative in nature and it should be expected that some or all of the assumptions underlying them will not materialize or will vary significantly from actual results. Accordingly, actual results will vary from the projections, and such variations may be material. Some important factors that could cause actual results to differ materially from those in any forward-looking statements contained in these materials include, without limitation, changes in interest rates, default and recovery rates, market, financial or legal uncertainties, the timing of acquisitions of loans, the types of loans acquired, differences in the actual allocation of loans from those assumed mismatches between the time of accrual and receipt of interest proceeds from the loans and whether or not and how loan investments may be leveraged.

Any statements involving matters of opinion or estimates, whether or not so expressly stated, are set forth as such and not as representations of fact, and no representation is made that such opinions or estimates will be realized. The statements and expressions of opinion contained in this presentation are subject to change without notice and involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon nor should they form the basis of an investment decision.

For Benefit Plan Investors

Not in limitation of the foregoing, if you are (or are acting on behalf of) a person that is a “benefit plan investor”, as defined in Section 3(42) of ERISA and DOL regulations (“Benefit Plan Investor”) you are not authorized to, and should not, rely on any information Antares is providing to you as a basis for, or otherwise in connection with, making a decision whether or not to invest with Antares. Antares has not provided and will not provide any investment advice of any kind whatsoever (whether impartial or otherwise) and Antares is not acting as a fiduciary, within the meaning of Section 3(21) of ERISA, and regulations thereunder, to the Benefit Plan Investor or to any fiduciary or other person making investment decisions on behalf of the Benefit Plan Investor, in connection with these materials or any related presentation.

Additional Matters and Important Information for All Non-U.S. Investors

An interest in products or services referenced in this presentation may not be licensed in all jurisdictions, and unless otherwise indicated, no regulator or government authority has reviewed this document or the merits of the products and services referenced herein. If you receive a copy of this presentation, you may not treat this as constituting a public or other offering and you should note that there may be restrictions or limitations to whom these materials may be made available. This presentation is directed at and intended for institutional investors (as such term is defined in the various jurisdictions). This presentation is provided on a confidential basis for informational purposes only and may not be reproduced in any form. Before acting on any information in this presentation, recipients should inform themselves of and observe all applicable laws and regulations of any relevant jurisdictions. Recipients should inform themselves as to the legal requirements and tax consequences within the countries of their citizenship, residence, domicile and place of business with respect to the ongoing provision of services, and any foreign exchange restrictions that may be relevant thereto. Antares does not accept any responsibility, nor can be held liable for any person’s use of or reliance on the information and opinions contained herein. Any entity responsible for forwarding this material to other parties takes responsibility for ensuring compliance with applicable securities laws.

Notice to persons in the European economic area and the United Kingdom

This presentation is being made available: (1) to persons in the European economic area only if they are professional investors as defined in the Alternative Investment Fund Managers Directive (2001/61/EU); and (2) to persons in the United Kingdom only if they are professional investors, as defined in the Alternative Fund Managers Regulations 2013 and fall within the following categories of exempt persons under the Financial Services and Market Act (Financial Promotion) Order 2005 (the “FPO”) and the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemptions) Order 2001 (the “CISPO”): (i) persons who are investment professionals, as defined in article 19(5) of the FPO and article 12(5)of the CISPO; (ii) persons who are high net worth companies, unincorporated associations etc., as defined in article 49(2)(a) to (d) of the FPO and article 22(2)(a) to (d) of the CISPO; or (iii) persons to whom it may otherwise lawfully be communicated. This presentation is provided for informational purposes only and does not constitute as offer to purchase, acquire, or subscribe for any type of investment